For years, India’s real-estate conversation has been dominated by the big metros. Mumbai, Delhi-NCR, Bengaluru, Hyderabad, and Pune have usually taken centre stage whenever the market moved. But that picture is beginning to change. A quieter, broader shift is now underway, and it is coming from beyond the metro skyline. Tier-2 cities are increasingly moving from the edge of the conversation to the middle of it. They are no longer being seen only as affordable alternatives to expensive metros. They are starting to look like genuine growth markets in their own right.

That does not mean every smaller city is suddenly booming in the same way. The reality is more nuanced. Some Tier-2 markets are showing strong buyer interest, land appreciation, and new commercial activity, while others are still evolving more slowly. But the overall direction is becoming harder to ignore. Recent reporting and industry research suggest that the next leg of India’s property growth may be shaped as much by smaller urban centres as by the traditional metro leaders.

One of the clearest reasons is affordability. In many metro markets, prices have risen so sharply in the post-pandemic years that a large section of end users has become more cautious. That is opening space for Tier-2 cities to attract attention. Business Standard reported earlier this year that smaller towns are expected to drive the next growth cycle in Indian housing as high prices in major cities begin to affect demand. In other words, the issue is not that homeownership dreams have disappeared. It is that many buyers are now looking for cities where those dreams still feel financially possible.

Affordability alone, however, is not enough to create a property story. What gives Tier-2 cities more credibility today is that several structural factors are beginning to support them at the same time. Infrastructure is improving, industrial corridors are expanding, digital connectivity is stronger, and local economies are becoming more diversified. Times of India recently highlighted a set of drivers behind non-metro real-estate growth, including better physical connectivity, government-backed urban development, remote work flexibility, and new employment opportunities. Together, these factors are changing how smaller cities are perceived by both buyers and investors.

The infrastructure angle matters especially because real estate responds strongly to access. Better roads, expressways, airports, freight corridors, and urban upgrades can change the investment profile of a city faster than almost anything else. Business Standard reported that land prices in Tier-2 and Tier-3 cities could rise sharply over the next two to four years as infrastructure projects and industrial expansion gather pace. The reported projections suggest increases of 25 percent to 100 percent in selected cities, with places such as Bhubaneswar, Cuttack, Erode, Puri, Varanasi, and Visakhapatnam being cited as likely beneficiaries. Whether every market delivers that kind of growth remains to be seen, but the direction of investor expectation is now very clear.

Another sign of this shift is that demand is no longer limited to only basic housing. In many Tier-2 locations, the market is becoming more layered. Younger professionals, first-time buyers, local business families, and returning NRIs are all shaping demand in different ways. Moneycontrol recently noted strong participation from first-time buyers in Tier-2 markets, supported by improving infrastructure and expanding job opportunities. At the same time, a Business Standard-linked release pointed to aspirational housing demand rising in smaller cities, driven by end users upgrading their primary homes rather than purely speculative buying. This mix matters because it suggests the market is not being driven by hype alone. It is being supported by real household decisions.

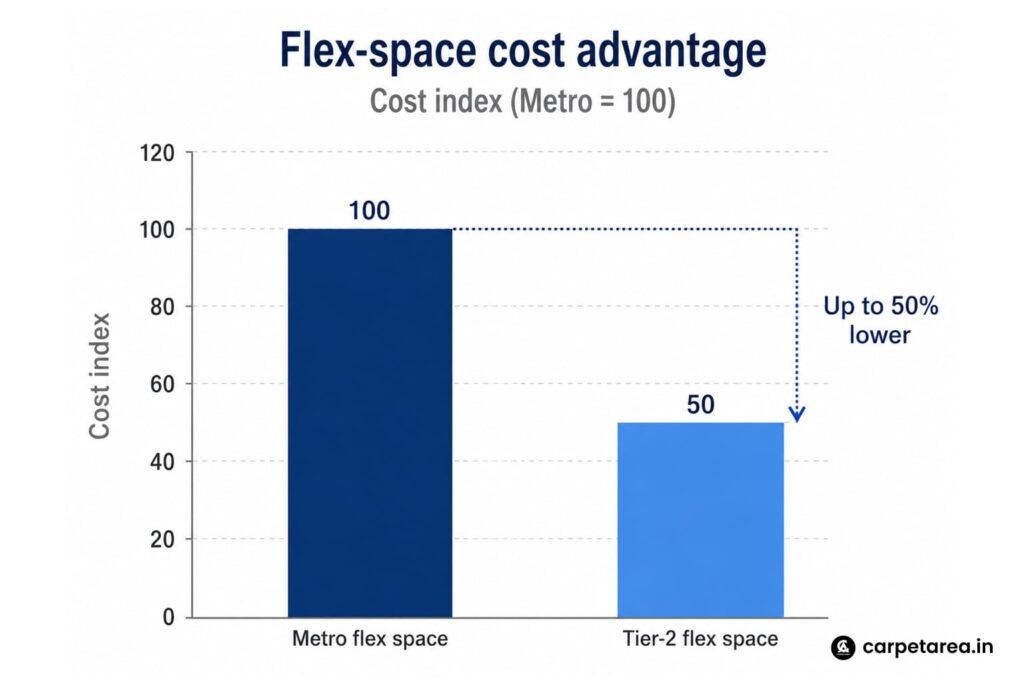

The commercial side of the story is becoming just as important. One of the old assumptions about smaller cities was that they could support residential growth but not serious office demand. That assumption is weakening. Economic Times reported that 17 smaller towns now house 575 co-working centres, and that flex spaces in Tier-2 cities can offer a cost advantage of up to 50 percent compared with metros. The same report said more than 200 companies have already established over 300 GCC bases across major Tier-2 cities. That is a meaningful signal because when office users move into smaller cities, housing, retail, and local services often move with them.

This does not mean metros are losing importance. They are still India’s biggest real-estate engines. But it does mean growth is spreading into a wider urban map. Colliers has already argued that multiple Tier-2 and Tier-3 cities are poised for faster activity across residential, office, industrial, and logistics segments. That kind of multi-sector attention is what turns a location from a low-cost alternative into a real growth corridor. The long-term importance of this shift is that India’s property future may become more distributed and less dependent on a handful of expensive metros.

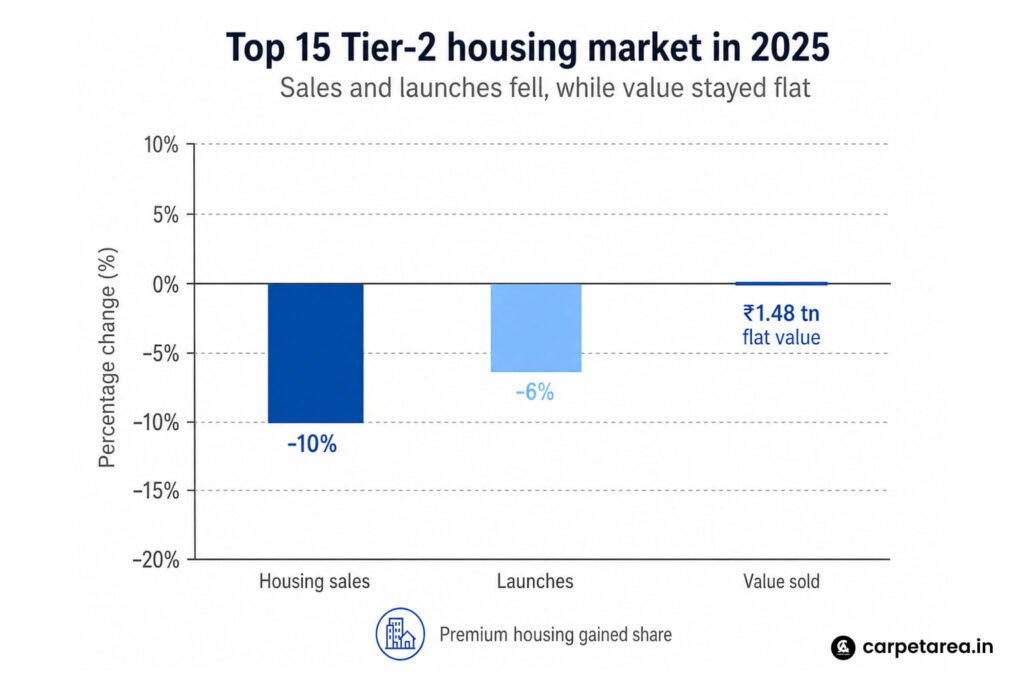

At the same time, this is not a simple one-way success story. There are important cautions here too. Business Standard reported in February that housing sales in the top 15 Tier-2 cities fell 10 percent in 2025, while launches fell 6 percent. That sounds like a contradiction to the broader growth narrative, but it actually tells a more useful story. It suggests that Tier-2 growth is real, but not effortless. Some markets are improving in value and quality even when sales volumes soften. The same report said the value of housing sold stayed flat at ₹1.48 trillion, while premium housing gained share. So the next cycle in smaller cities may not be only about more units. It may be about better projects, evolving buyer preferences, and stronger value concentration.

That distinction is important for buyers. A Tier-2 city is not automatically a good real-estate bet just because it is cheaper than a metro. The right question is whether the city has enough economic energy, infrastructure momentum, and job creation to support long-term demand. A lower entry price can attract attention, but sustainable value growth usually comes from deeper fundamentals such as connectivity, industry, education, healthcare, and a rising employment base. The most promising cities are the ones where these pieces are starting to come together at the same time. This is an inference supported by the infrastructure, office, and urban-development trends reported across sources.

For developers, Tier-2 cities now offer both opportunity and challenge. The opportunity is obvious: land is often less expensive, buyer interest is rising, and competition can still be lighter than in crowded metro markets. But the challenge is that buyers in these cities are also becoming more aware and more selective. They expect better design, stronger amenities, and more credible delivery. That means developers cannot assume that lower-cost projects alone will win. In many places, the successful product will be the one that matches local aspirations with disciplined pricing and real livability. The premium-housing shift noted in recent reports points to exactly this kind of market evolution.

For investors, the attraction is different. Tier-2 cities offer the possibility of entering a market before it becomes fully priced in. That is why land and plotted development stories often get so much attention in these locations. But early-stage opportunity also comes with higher selection risk. Not every emerging city becomes a breakout market. Some may benefit quickly from one infrastructure project, while others may take much longer to build lasting demand. The best opportunities are likely to be in cities where multiple drivers overlap: infrastructure, industrial activity, office demand, and stable end-user housing absorption.

What makes the Tier-2 trend especially important right now is timing. India’s larger housing market is entering a more selective phase. In such an environment, smaller cities with sensible pricing, improving connectivity, and rising local demand can start to look far more attractive than overheated urban pockets where affordability is badly stretched. That does not mean the next growth story will belong only to Tier-2 cities. But it does mean they are no longer secondary characters in India’s real-estate future.

In the end, the real story is not simply that Tier-2 cities are growing. It is that they are maturing. They are becoming more connected, more investable, and more central to the way India’s urban expansion is unfolding. Some will move faster than others, and some will still disappoint. But the broader shift is real. The next meaningful real-estate cycle in India may not come only from the usual metros. It may come from the cities that were once seen as alternatives and are now starting to look like destinations in their own right.

Leave a Reply