For many people, this question does not begin with a spreadsheet. It begins with a feeling.

It starts when the landlord increases the rent again. Or when a friend books a flat and suddenly the family starts asking, “How long will you keep paying rent?” Sometimes the question comes after marriage. Sometimes after a child is born. Sometimes after years of shifting from one apartment to another and never feeling fully settled.

That is when the real estate debate becomes personal: should you buy a home, or should you continue living on rent?

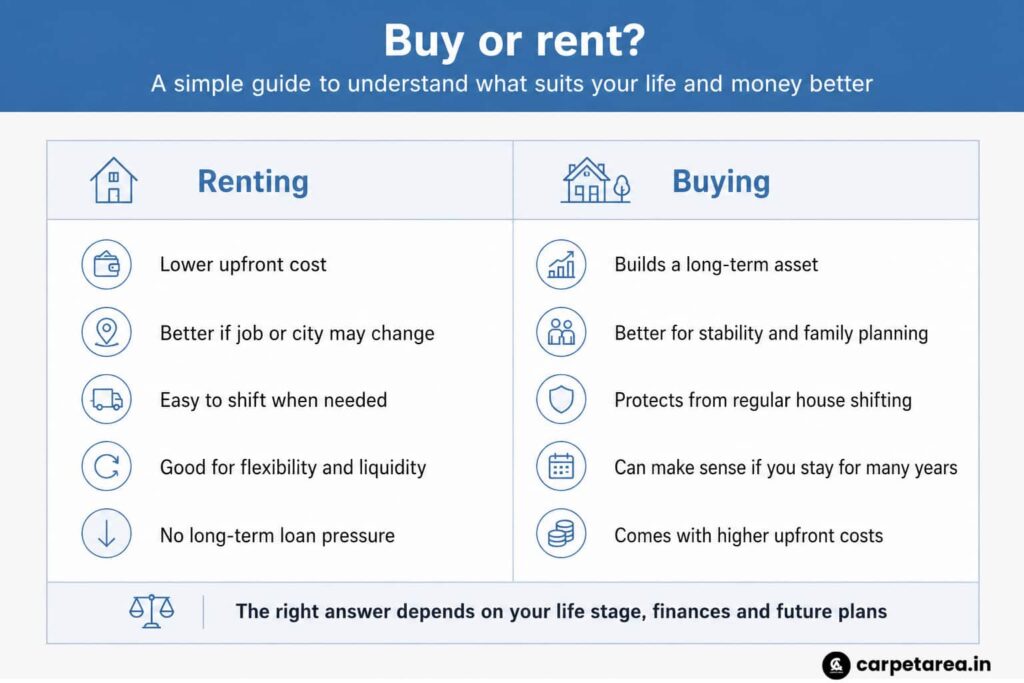

The problem is that this decision is often explained in a very simplistic way. Some people say rent is wasted money, so buying is always better. Others say buying creates pressure, so renting is always smarter. But life is rarely that black and white. A home is not just a financial decision. It is also a life decision. It affects stability, mobility, savings, stress, family planning, and peace of mind.

That is why the right question is not which option sounds better in general. The right question is which option makes more sense for your stage of life right now.

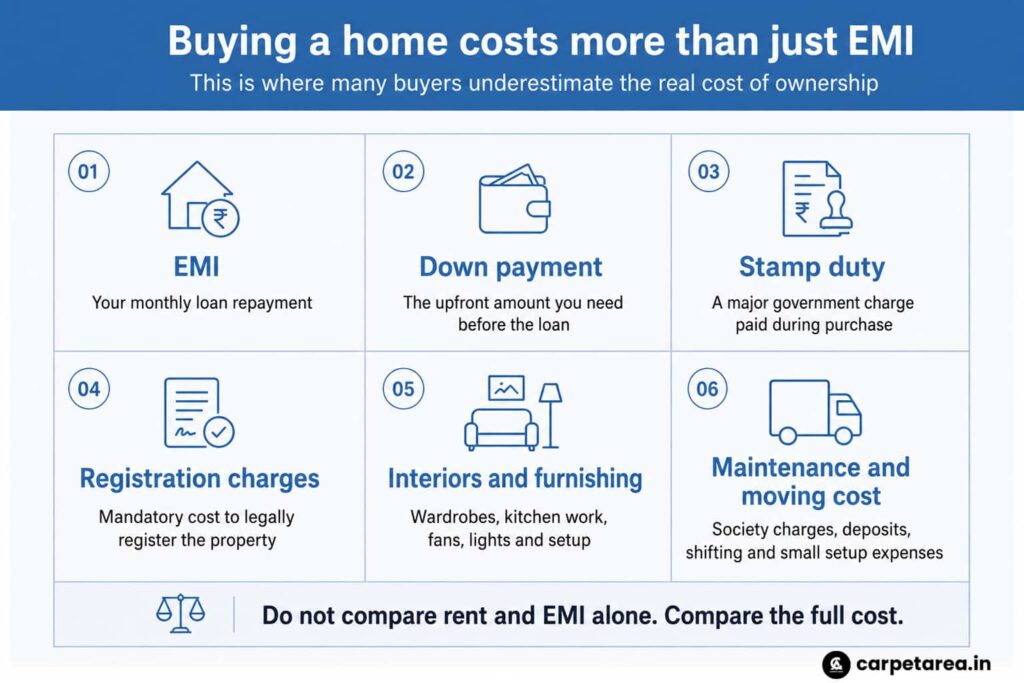

One of the biggest mistakes people make is comparing only rent and EMI.

A person paying monthly rent looks at a possible home loan EMI and thinks, at least the EMI will help build an asset. On the surface, that sounds reasonable. But buying a home is never just about the EMI.

The day you decide to buy, many other costs enter the picture. There is the down payment. There are government charges like stamp duty and registration. There may be loan processing fees. There may be interior work, wardrobe fittings, modular kitchen costs, lighting, shifting expenses, maintenance deposits, and society charges. These costs are often not discussed enough when people casually compare rent and EMI.

That is where many first-time buyers get confused. They compare one monthly number with another monthly number and forget that ownership begins with a much bigger financial event.

The smarter comparison is not rent versus EMI. It is rent versus the full cost of ownership.

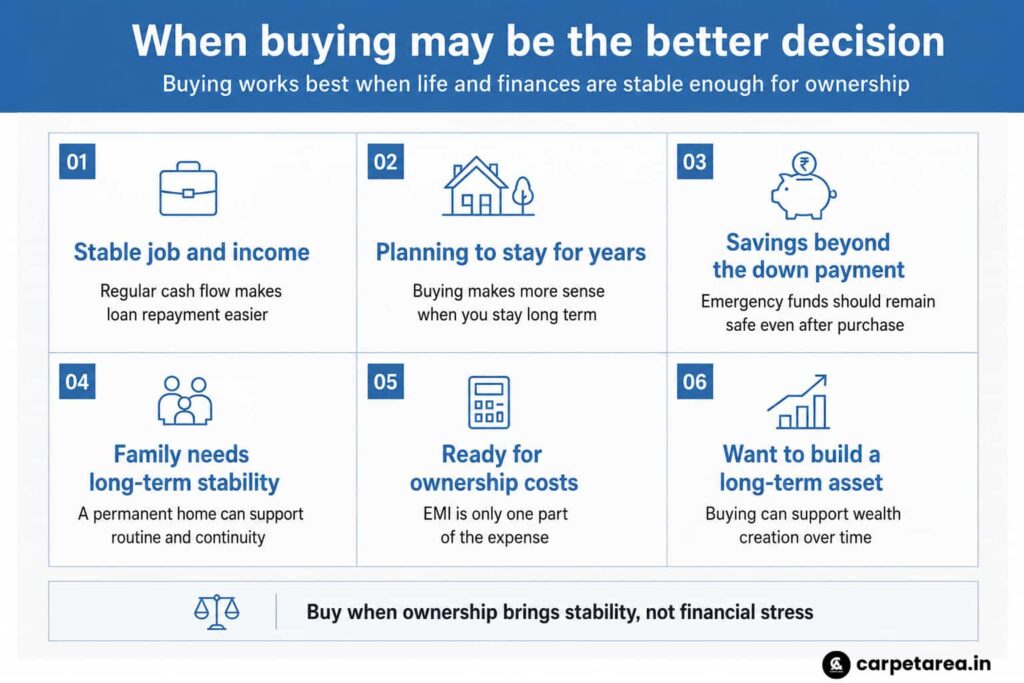

Buying usually makes more sense when life has become stable enough to support it.

If your income is steady, your city is likely to remain the same for the next several years, and you have enough savings to handle not just the down payment but also the extra buying costs, then ownership can become a strong long-term decision. In that situation, buying is not only about owning walls and a roof. It is about creating certainty.

A permanent home can bring a different kind of comfort to a family. Children may get continuity. Parents may feel more settled. You may stop worrying about shifting again and again. Even simple things, like knowing your address is not temporary, can make life feel more stable.

But buying should not happen only because of pressure. It should happen when the home fits your real life for the long term. If your job, family plans, and location preference all support staying put, then ownership can make emotional and financial sense.

At the same time, a buyer should be realistic. A home loan is a long responsibility, not a short excitement. If income is tight or future plans are uncertain, ownership can start feeling less like stability and more like strain.

That is why buying works best when stability is already present in life, not when a person is hoping the purchase itself will create stability.

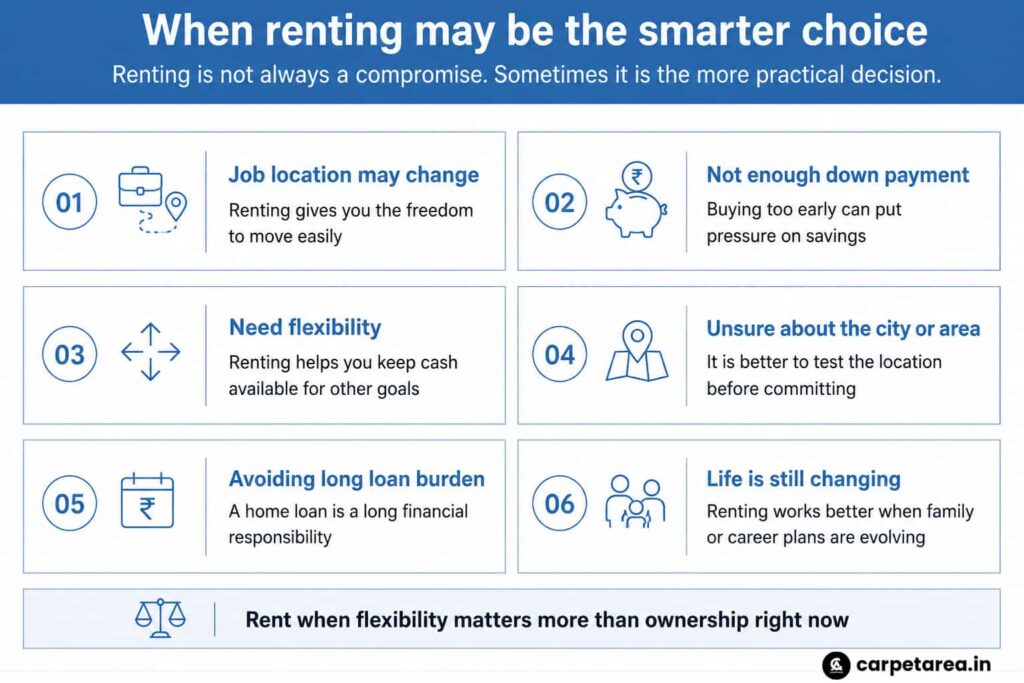

Renting, on the other hand, is often treated unfairly. Many people talk about it as if it is only a temporary compromise. In reality, renting can be a very practical and intelligent choice.

If your career is still evolving, if your city may change, if you are unsure about the area you want to settle in, or if buying today would stretch your finances too hard, then renting may actually be the wiser option. Rent gives you flexibility. It helps preserve cash. It allows you to test a city, a location, and even a lifestyle before making a long commitment.

There is also a truth people do not always say openly. Many buyers are not financially ready to own, but feel socially pushed to buy. They dip too deeply into savings, underestimate the hidden costs, and then spend years carrying financial stress that affects the rest of life.

In such cases, rent is not wasted money. It is the cost of flexibility, breathing space, and reduced pressure.

Renting also makes sense when you do not want to lock yourself into one city too early. In a changing phase of life, mobility itself has value. Sometimes the ability to move easily is worth more than the satisfaction of ownership.

The most important question underneath this entire debate is simple: how long are you likely to stay where you are?

This is where the answer becomes clearer.

If you are confident that your work, family, and future plans are connected to the same city for many years, buying becomes easier to justify. The one-time buying costs get spread over a longer period of actual use. The emotional value of ownership also becomes more meaningful.

But if you are unsure about your city, your job path, your family size, or even the kind of home you really want, buying too early can lock you into the wrong decision. In that case, rent does not just give you shelter. It gives you time. And in real estate, time can be just as valuable as money.

Before choosing between buying and renting, it helps to ask a few honest questions.

Can I make the down payment and still keep an emergency fund safe?

Can I handle registration, stamp duty, interiors, and moving expenses without stress?

Am I likely to stay in this city and this area for the next several years?

If my monthly financial burden rises later, will I still be comfortable?

Am I buying because it truly suits my life, or because I feel I should buy by now?

These questions are more useful than any dramatic advice on social media. Because the best property decisions are not made by pressure. They are made by clarity.

So what should a person actually do?

A person should buy when life is stable, finances are strong, and the home solves a real long-term need.

A person should rent when flexibility matters, savings need to stay free, or buying would create more stress than comfort.

That may not sound like a dramatic answer, but it is the honest one.

Both choices can be right. Renting can protect your freedom. Buying can anchor your future. The smarter decision is the one that matches your present life, not the one that sounds more impressive in conversation.

And perhaps that is the most important real estate lesson of all. A home should not become a burden carried for social approval. It should become a decision taken with patience, self-awareness, and calm thinking.

Sources:-

NHB RESIDEX press release: https://www.nhb.org.in/wp-content/uploads/2026/03/National-Press-Release-RESIDEX-Dec25-DV002.pdf

RBI home loan FAQs: https://www.rbi.org.in/commonperson/english/scripts/FAQs.aspx?Id=701

RBI floating-rate reset FAQs: https://www.rbi.org.in/commonperson/English/scripts/FAQs.aspx?Id=3687

Delhi Revenue property registration: https://revenue.delhi.gov.in/revenue/property-registration

Reuters market affordability report: https://www.reuters.com/world/india/indias-luxury-housing-boom-lift-home-prices-squeezing-affordability-further-2026-03-12/

Leave a Reply