Flexible workspaces were once seen as temporary offices for freelancers, early-stage startups and small teams. That image is now outdated. In India’s commercial real estate market, flex spaces are moving from the edge of the office sector to the centre of corporate strategy. Large companies, GCCs, startups, consulting firms, technology teams and growing enterprises are now using flexible offices not as a backup option, but as a serious real estate solution.

The biggest reason is the changing nature of work. Companies no longer want every office decision to be fixed for five, seven or ten years. Teams are expanding, shrinking, relocating and restructuring faster than before. Hybrid work has also changed how companies use office space. Instead of taking large permanent offices everywhere, many occupiers now prefer managed spaces where they can scale seats, control costs and enter premium business districts quickly.

This is why flexible workspaces are becoming a key asset class in India’s commercial real estate market. Reports show that flex offices have evolved from niche setups into a mainstream segment because enterprises now want agility, cost efficiency and employee-friendly work environments. The demand is no longer only from startups. Large corporates are also using flexible spaces for project teams, satellite offices, temporary expansion, client-facing teams and hybrid work models.

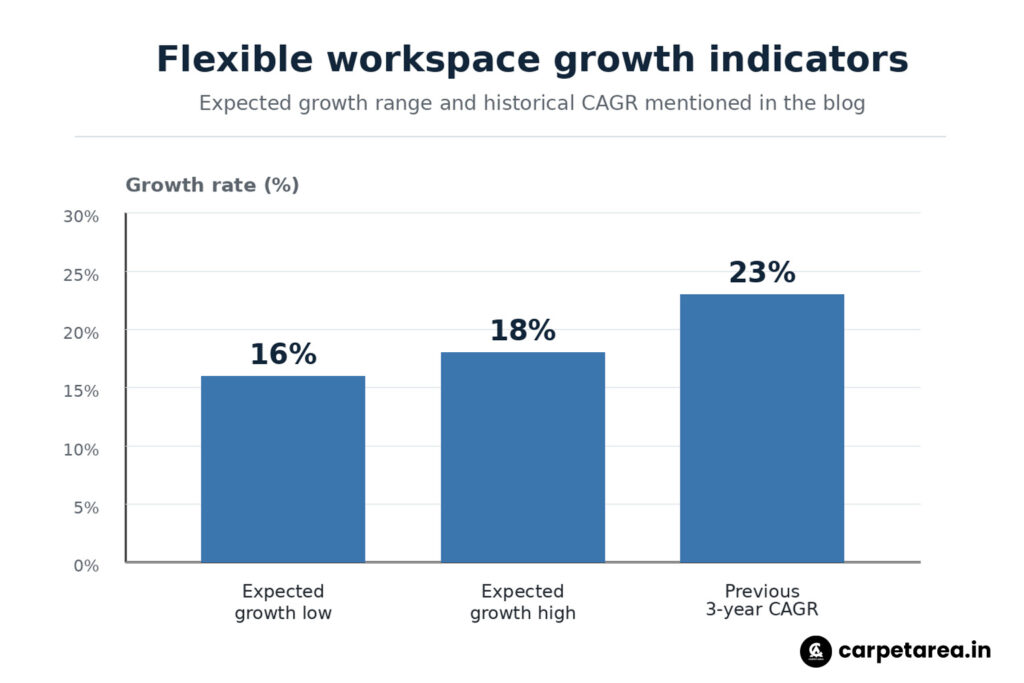

The numbers show how serious this shift has become. Crisil expects India’s flexible workspace market to expand by 16% to 18% over the current and next fiscal year, reaching total capacity of around 140 to 145 million sq ft. The report also says the segment had already grown at a strong 23% compound annual growth rate over the previous three fiscal years leading up to FY2026. That is not a small side trend. It is a structural shift in how offices are being consumed.

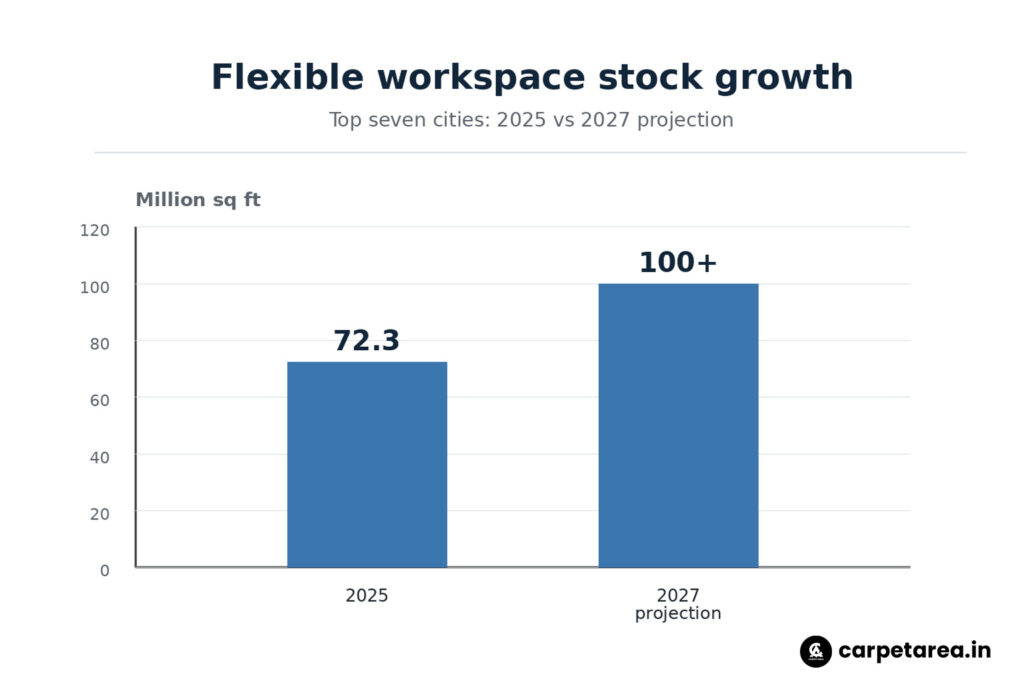

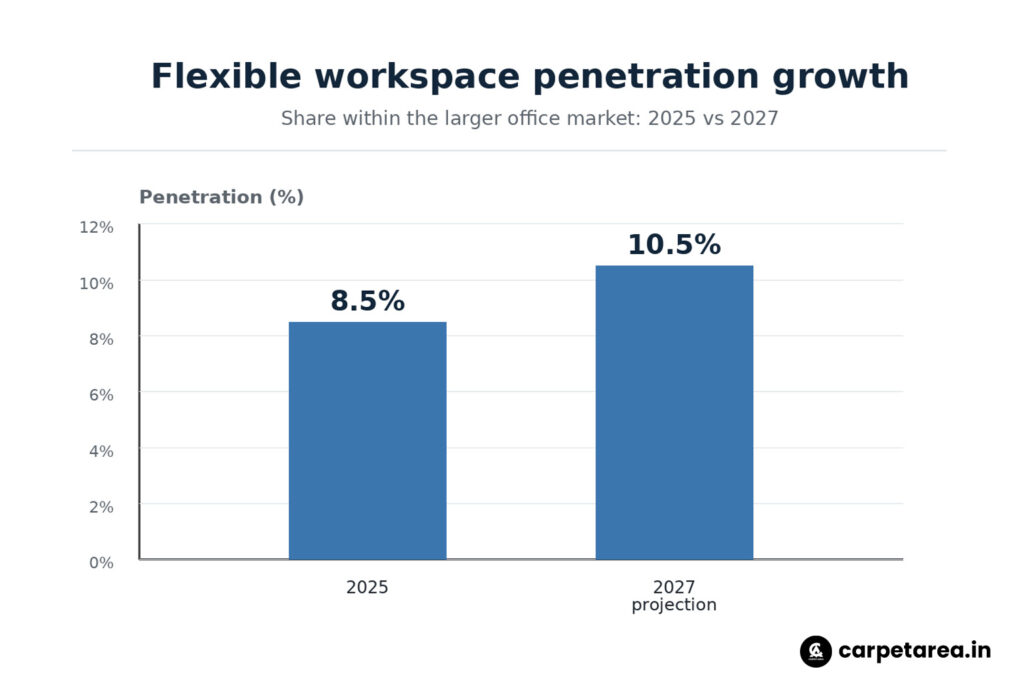

Colliers has also projected strong growth for the sector. Its report said flex stock across India’s top seven cities is expected to cross 100 million sq ft by 2027, up from 72.3 million sq ft in 2025. Flex penetration is also expected to rise from 8.5% in 2025 to 10.5% by 2027. This means flexible workspaces are not just growing in absolute size. Their share within the larger office market is also increasing.

For developers and landlords, this is important because flex operators are becoming serious office occupiers. Earlier, a building owner may have preferred only traditional corporate tenants. Today, a strong flex operator can become an anchor tenant in a commercial building. It can lease large areas, improve occupancy, create ready-to-use office formats and attract many smaller occupiers into one property.

This model also helps landlords reduce vacancy risk. Instead of waiting for one large company to lease an entire floor or tower, a flex operator can take space and then distribute it across multiple users. That creates a different kind of demand engine inside the building. If managed properly, flex spaces can make an office asset more active, more adaptable and more attractive to modern occupiers.

For companies, the benefit is speed. Setting up a traditional office requires lease negotiation, fit-outs, furniture, IT infrastructure, maintenance, security, compliance and facility management. A managed flexible workspace reduces that burden. A company can move faster, open a new location with less capital expenditure and adjust space requirements as business needs change.

This is especially relevant for GCCs. India’s GCC ecosystem is expanding rapidly, and many global companies need high-quality office space without delay. Flexible offices allow them to start operations quickly, test a city, hire teams and later decide whether they want a larger long-term campus. Crisil’s outlook also connects the growth of flex workspaces with demand from GCCs and startups.

The trend is visible in real transactions as well. Awfis recently expanded in Chennai by leasing over 110,000 sq ft across two new centres, taking its Chennai footprint to 28 centres across 8.75 lakh sq ft. Such expansions show that flex operators are no longer operating only in Bengaluru, Gurugram or Mumbai. They are deepening their presence in large office markets and also entering newer business corridors.

Another example is Bengaluru, where BHIVE leased around 1.4 lakh sq ft of Grade-A office space from Concorde, with the lease reportedly valued at about ₹16 crore in annual rentals. This shows that flex and managed office operators are participating in large-format commercial leasing, not just small co-working centres.

For investors, the message is clear. Flexible workspace is becoming an investable commercial real estate theme. It is linked to enterprise demand, office leasing, workplace experience, managed services and recurring rental income. Colliers’ 2026 outlook also said flexible workspaces are expected to account for nearly 20% of Grade-A leasing in 2026, supported by hybrid work, cost optimisation and speed-to-market requirements.

But this does not mean every flex space will succeed. Location still matters. Grade-A buildings, metro connectivity, business districts, parking, building quality, technology infrastructure and operator credibility are critical. A poorly located flex centre with weak management can struggle, even if the overall sector is growing.

There is also an important difference between co-working and managed office space. Co-working usually refers to shared seats, open desks and smaller users. Managed offices are more customised for enterprises, with dedicated floors, private cabins, meeting rooms, branding, access control and technology support. The strongest growth is coming from the enterprise-grade managed office segment, where companies want flexibility without compromising professionalism.

For commercial property owners, the opportunity is to design buildings that can support this new demand. Flexible floor plates, better common areas, strong internet backbone, ESG compliance, food and beverage access, wellness zones and high-quality facility management can make an office building more attractive to flex operators and enterprise tenants.

For Carpet Area readers, the takeaway is simple. Flexible workspaces are no longer a temporary trend created by the pandemic. They are becoming a permanent part of India’s commercial real estate structure. Companies want agility. Employees want better workplace experience. Developers want stronger occupancy. Investors want scalable income-generating assets.

In simple words, the office market is shifting from fixed space to flexible strategy. The winners will be those buildings, operators and investors that understand this change early. Flexible workspaces are not replacing traditional offices completely, but they are becoming one of the most important ways companies use office real estate in India.

Leave a Reply