India’s luxury housing market is entering a more selective phase, but that does not mean demand has disappeared. In fact, the latest guidance from DLF suggests that the top end of the market is still active, especially when the project has the right brand, location and product positioning.

DLF is targeting around ₹20,000 crore in sales bookings in FY27, broadly similar to its FY26 sales trajectory. The company’s launch pipeline is focused on premium residential projects across Gurugram, Mumbai and Goa, three markets that represent different luxury buyer categories: NCR high-income professionals, Mumbai premium urban buyers, and Goa second-home or lifestyle buyers.

This number is important because DLF is not chasing volume in a low-price market. Its focus is on high-value luxury housing where buyer expectations are very different. A premium buyer is not only looking for a flat. The buyer is looking for location, privacy, branded delivery, open spaces, design quality, maintenance standard, security and long-term asset value.

The ₹20,000 crore FY27 target also has a clearer structure. According to DLF management commentary reported by Economic Times, around ₹14,000 to ₹15,000 crore of the expected sales may come from new launches planned during FY27, while the remaining sales are likely to come from The Dahlias in Gurugram. This makes the target more believable because it is not dependent on one single fresh launch. It is a mix of new projects and continuing sales from an already successful ultra-luxury project.

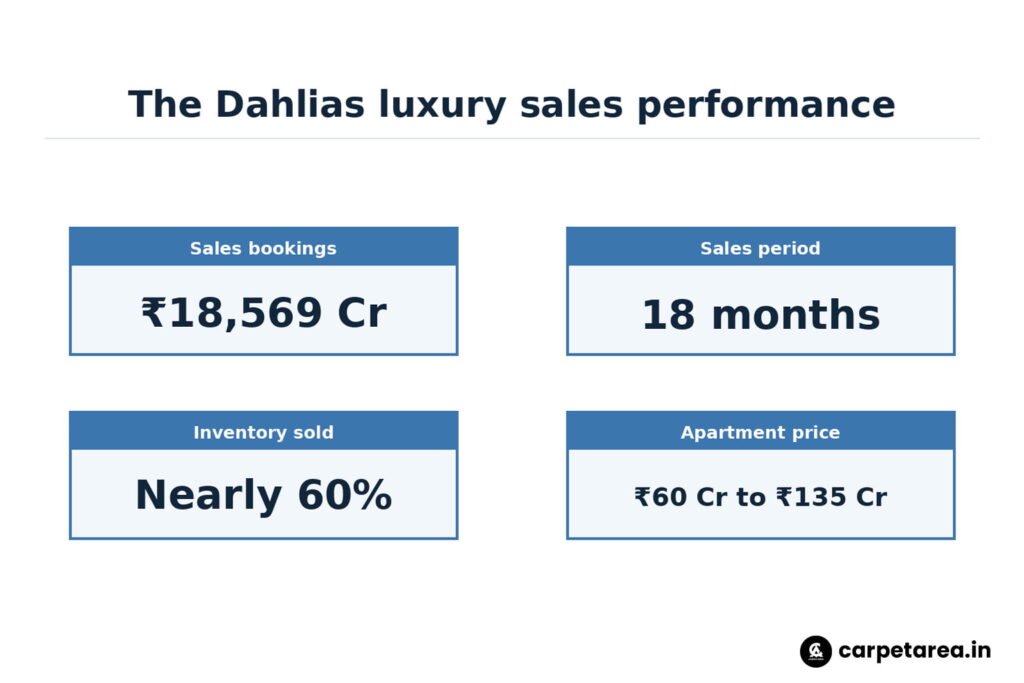

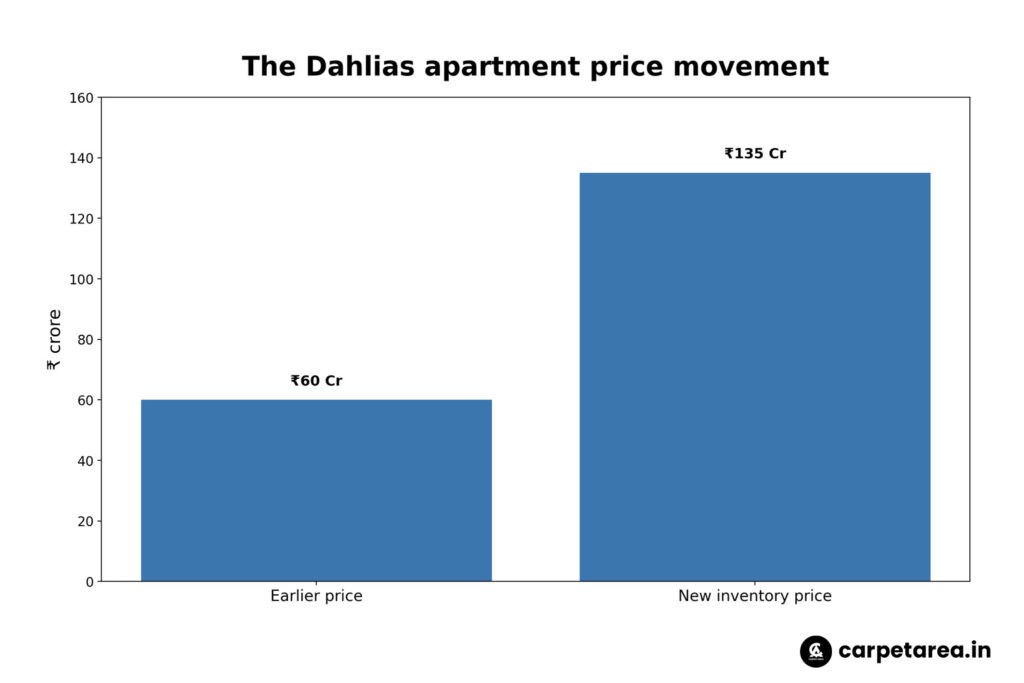

The Dahlias is central to this story. The project has reportedly recorded ₹18,569 crore in sales bookings within 18 months, with nearly 60% of inventory already sold. Apartment prices have reportedly moved from around ₹60 crore earlier to nearly ₹135 crore for new inventory, showing the depth of demand in the ultra-luxury category when location and brand confidence are strong.

This is not ordinary housing demand. It is a very specific luxury demand coming from buyers who are willing to pay for scarcity, lifestyle and status. Such demand is usually concentrated in a few strong micro-markets. That is why Gurugram remains so important for DLF. The city has a large base of corporate leadership, entrepreneurs, HNIs, NRIs and high-income households. It also has established premium corridors where luxury projects can command very high ticket sizes.

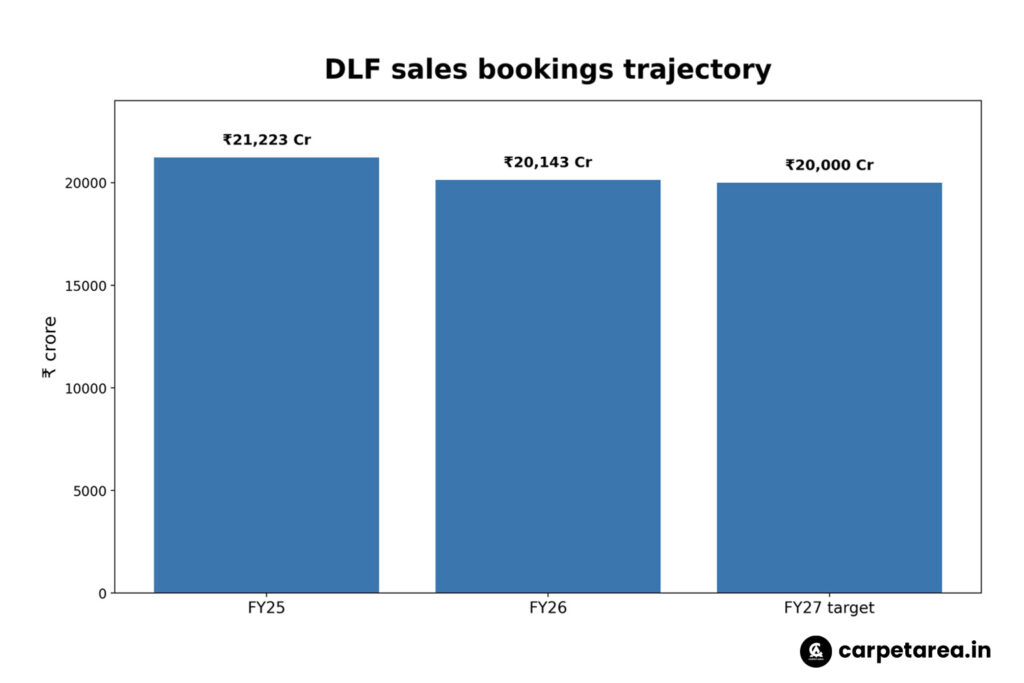

DLF’s FY26 base also makes the FY27 guidance meaningful. In FY26, DLF’s sales bookings were ₹20,143 crore, down 5% from the record ₹21,223 crore achieved in FY25. So the FY27 target is not a sudden jump. It is an attempt to maintain a high booking level in a more selective market.

This is where the story becomes important for the larger real estate market. Luxury housing demand may remain strong, but it is not unlimited. Buyers are becoming more careful. They are comparing developer credibility, location strength, design quality, delivery record and resale potential. In this environment, large listed developers have an advantage because buyers trust stronger balance sheets and better execution histories.

DLF’s management has also indicated that the company is not trying to chase pre-sales just for the sake of headline numbers. The focus is on margins, cash generation and disciplined execution rather than aggressive volume chasing. That is a healthier signal for the market because it suggests that top developers are trying to maintain quality and financial discipline.

For homebuyers, the lesson is simple. Luxury projects should not be judged only by brochure appeal. Buyers should check RERA details, approvals, total cost, maintenance charges, delivery timeline, carpet area, payment schedule and the developer’s obligations. In ultra-luxury housing, even a small percentage cost can translate into a large rupee amount.

For investors, the message is also clear. DLF’s ₹20,000 crore FY27 plan shows confidence in premium housing, but it does not mean every luxury project in every city will perform well. The real opportunity is selective. Strong brands, strong corridors and limited high-quality inventory may continue to do well. Weak locations or over-priced projects may not get the same response.

This is where the story becomes important for the larger real estate market. Luxury housing demand may remain strong, but it is not unlimited. Buyers are becoming more careful. They are comparing developer credibility, location strength, design quality, delivery record and resale potential. In this environment, large listed developers have an advantage because buyers trust stronger balance sheets and better execution histories.

DLF’s management has also indicated that the company is not trying to chase pre-sales just for the sake of headline numbers. The focus is on margins, cash generation and disciplined execution rather than aggressive volume chasing. That is a healthier signal for the market because it suggests that top developers are trying to maintain quality and financial discipline.

For homebuyers, the lesson is simple. Luxury projects should not be judged only by brochure appeal. Buyers should check RERA details, approvals, total cost, maintenance charges, delivery timeline, carpet area, payment schedule and the developer’s obligations. In ultra-luxury housing, even a small percentage cost can translate into a large rupee amount.

For investors, the message is also clear. DLF’s ₹20,000 crore FY27 plan shows confidence in premium housing, but it does not mean every luxury project in every city will perform well. The real opportunity is selective. Strong brands, strong corridors and limited high-quality inventory may continue to do well. Weak locations or over-priced projects may not get the same response.

In simple words, DLF’s FY27 launch plan tells us that India’s luxury housing market is still strong, but more focused. Buyers are ready to pay, but they want credibility, scarcity, lifestyle and long-term value. The success of The Dahlias gives DLF confidence, while the planned launches in Gurugram, Mumbai and Goa show where the company sees future demand.

The larger takeaway is this: premium housing is not slowing down everywhere. It is becoming more selective. For serious buyers and investors, that means the question is no longer “is luxury housing growing?” The better question is: “which luxury projects, in which locations, by which developers, are strong enough to justify the price?”

Optional source line for blog:

Sources: Economic Times / ET Realty and Hindustan Times reports on DLF’s FY27 sales guidance, launch pipeline across Gurugram, Mumbai and Goa, and The Dahlias sales performance.

Leave a Reply