Buying a ₹50 lakh home looks simple on paper.

The buyer sees the property price, opens an EMI calculator and starts thinking about loan approval. But a home is not bought only with EMI.

A ₹50 lakh home also requires:

- down payment,

- stamp duty,

- registration charges,

- interiors,

- shifting expenses,

- emergency savings,

- maintenance costs,

- and enough monthly income to manage the loan without disturbing family life.

This is where many buyers make the wrong calculation.

They ask:

Will the bank approve my home loan?

But the more important question is:

Can my family comfortably live with this EMI for the next 15 to 25 years?

A bank may approve a loan based on salary, credit score, age and repayment capacity. However, only the buyer knows the actual pressure created by school fees, healthcare expenses, existing loans, family responsibilities, job uncertainty and monthly household costs.

The correct home-buying decision must therefore go beyond loan eligibility.

Why does affordability matter before buying a home?

A ₹50 lakh property does not usually mean a ₹50 lakh loan.

In most cases, the buyer must arrange part of the property price from personal savings. If the buyer pays 20% as down payment, the approximate structure may look like this:

| Cost item | Approximate amount |

|---|---|

| Property price | ₹50 lakh |

| Down payment at 20% | ₹10 lakh |

| Home loan amount | ₹40 lakh |

| Stamp duty and registration | Extra |

| Interiors and shifting | Extra |

| Emergency fund | Extra |

The most important point is that a ₹50 lakh home usually requires more than ₹10 lakh of cash readiness.

The down payment is only one part of the upfront requirement. Stamp duty, registration, brokerage where applicable, interiors, appliances and moving expenses may not be fully covered by the home loan.

This is why buyers should not empty their entire savings account only to make the down payment.

A home may be financially affordable on paper but become stressful if the buyer has no emergency reserves left after possession.

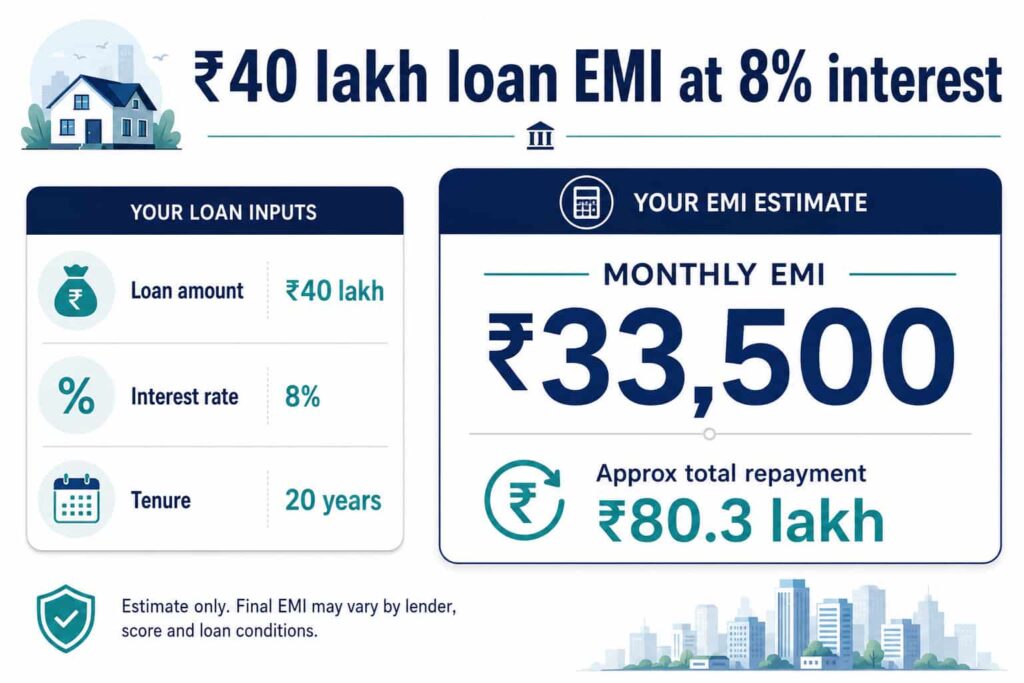

What is the EMI on a ₹40 lakh home loan?

Let us take a practical example.

| Assumption | Detail |

| Property price | ₹50 lakh |

| Down payment | ₹10 lakh |

| Home loan amount | ₹40 lakh |

| Interest rate assumption | 8% per annum |

| Loan tenure | 20 years |

| Approximate EMI | ₹33,500 per month |

At around 8% annual interest for 20 years, the monthly EMI on a ₹40 lakh home loan is approximately ₹33,500.

The final EMI may differ depending on:

- the lender,

- credit score,

- employment type,

- loan tenure,

- fixed or floating rate,

- processing terms,

- and the interest rate applicable at the time of sanction.

The buyer should also remember that ₹33,500 is not the complete monthly housing cost.

Society maintenance, property tax, insurance, repair expenses, utility bills and travel costs may increase the actual monthly burden.

How much salary is needed for a ₹50 lakh home?

A useful way to judge affordability is to compare EMI with monthly income.

If a large part of income goes into one loan, the family may struggle to save for emergencies, retirement, children’s education or medical needs.

For an EMI of approximately ₹33,500, the salary requirement may look like this:

| EMI as a percentage of income | Approximate monthly salary required |

| EMI at 35% of income | ₹96,000 |

| EMI at 40% of income | ₹84,000 |

| EMI at 45% of income | ₹74,500 |

The practical range is therefore:

A buyer may need approximately ₹80,000 to ₹1 lakh of monthly income to comfortably consider a ₹50 lakh home with a ₹40 lakh loan.

This is not a universal rule.

A buyer earning less may still qualify if:

- the down payment is higher,

- the loan amount is lower,

- there is a co-applicant,

- existing debt is minimal,

- household expenses are low,

- or savings are strong.

Similarly, a buyer earning more may still feel pressure if there are several existing obligations.

Why should buyers avoid using the maximum loan eligibility?

Banks calculate eligibility based on measurable financial data.

The family experiences affordability based on real life.

These are not the same thing.

A bank may approve a high loan amount because the applicant has a stable salary and good credit score. But the bank does not fully measure the emotional and practical impact of:

- children’s education,

- parents’ healthcare,

- medical emergencies,

- job changes,

- planned retirement,

- vehicle loans,

- personal loans,

- or future lifestyle needs.

A buyer should never assume that the maximum sanctioned amount is automatically the right amount to borrow.

The safer approach is to keep the EMI at a level that leaves room for savings and unexpected expenses.

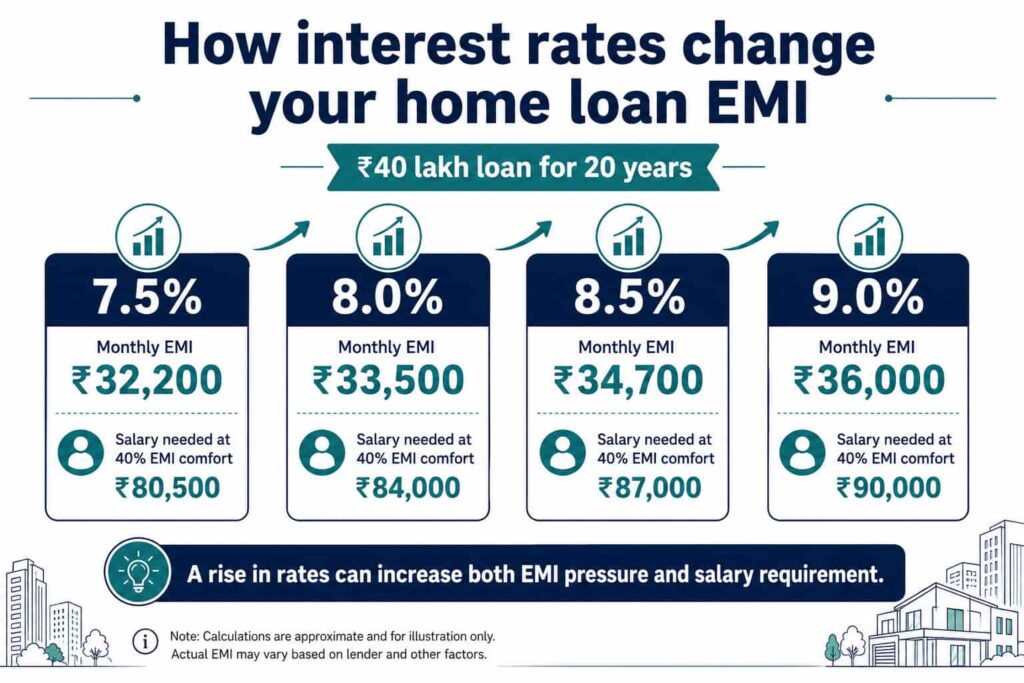

How can interest rates change the EMI?

A small increase in interest rate can significantly change the monthly EMI over a long tenure.

For a ₹40 lakh home loan over 20 years, the approximate impact may look like this:

| Interest rate | Approximate EMI | Salary needed at 40% EMI comfort |

| 7.5% | ₹32,200 | ₹80,500 |

| 8.0% | ₹33,500 | ₹84,000 |

| 8.5% | ₹34,700 | ₹87,000 |

| 9.0% | ₹36,000 | ₹90,000 |

A buyer comfortable at 7.5% may begin feeling pressure if the rate moves towards 9%.

A rate increase can affect the borrower in two ways:

- The EMI may rise.

- The loan tenure may increase if the EMI remains unchanged.

Both outcomes can affect long-term financial planning.

That is why a buyer should not calculate affordability using only the lowest available rate.

A safer calculation includes an interest-rate buffer.

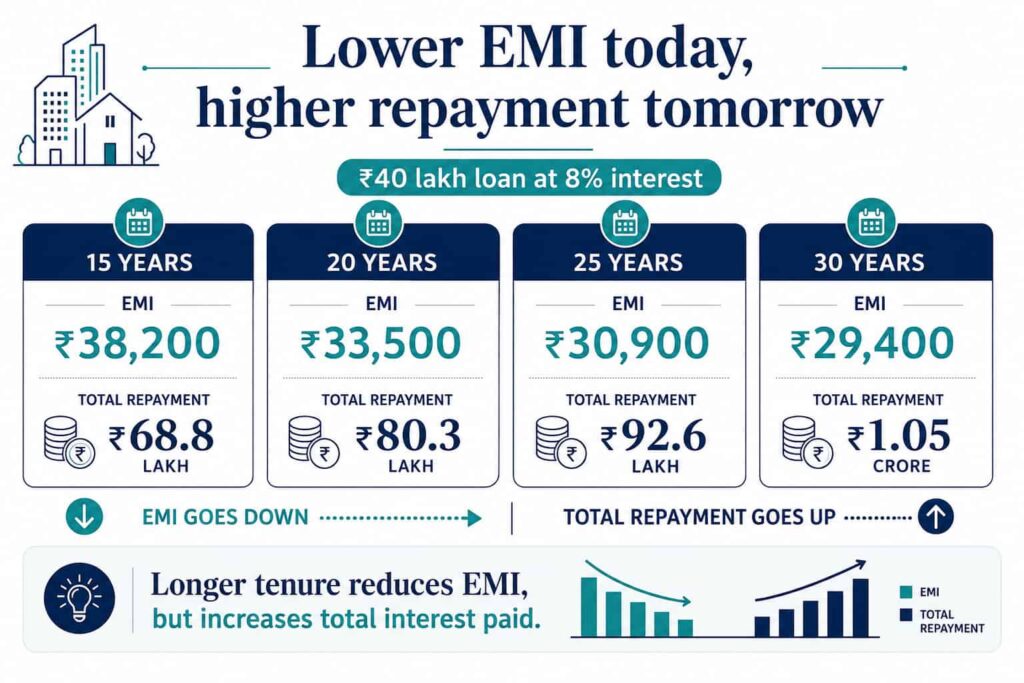

Longer tenure reduces EMI but increases total repayment

Many buyers choose a longer tenure because it lowers the monthly EMI.

This may improve immediate affordability, but it increases the total amount paid to the bank.

For a ₹40 lakh loan at 8% interest, the approximate comparison is:

| Loan tenure | Approximate EMI | Approximate total repayment |

| 15 years | ₹38,200 | ₹68.8 lakh |

| 20 years | ₹33,500 | ₹80.3 lakh |

| 25 years | ₹30,900 | ₹92.6 lakh |

| 30 years | ₹29,400 | ₹1.05 crore |

The difference between a 15-year and a 30-year loan is significant.

The 30-year loan reduces the EMI by less than ₹9,000 per month compared with the 15-year option, but the total repayment increases by more than ₹36 lakh.

A longer tenure may still be useful for buyers who need monthly flexibility. However, they should consider prepayments whenever income improves.

The right tenure should balance:

- monthly comfort,

- total interest,

- expected career growth,

- retirement age,

- and the ability to make future prepayments.

Bank eligibility is not the same as family affordability

Banks examine factors such as:

- income,

- age,

- employment stability,

- credit score,

- property value,

- repayment history,

- and existing loans.

These factors help the lender estimate repayment risk.

The family must examine a wider financial picture.

Bank eligibility checks

- Salary or business income

- Age

- Credit score

- Existing liabilities

- Employment profile

- Property valuation

Family affordability checks

- Household expenses

- School fees

- Medical costs

- Insurance

- Emergency savings

- Parents’ support

- Lifestyle costs

- Job uncertainty

- Future financial goals

A buyer can be eligible for a loan and still be financially unprepared for homeownership.

The correct question is not only whether the EMI can be paid this month.

The buyer should ask whether the family can continue paying it during:

- a job change,

- temporary income reduction,

- medical emergency,

- maternity break,

- business slowdown,

- or a rise in interest rates.

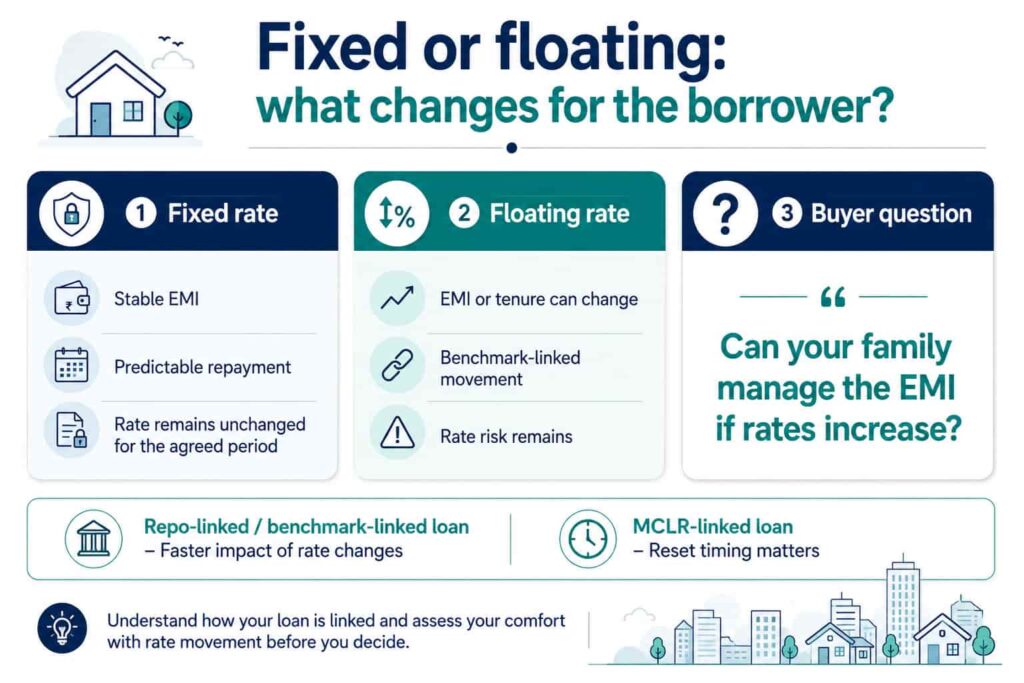

Fixed or floating home loan rate?

Before taking a home loan, buyers should understand how the interest rate works.

| Loan rate type | Meaning | Buyer impact |

| Fixed rate | Rate remains unchanged for the agreed period | Greater EMI predictability |

| Floating rate | Rate changes with benchmark movement | EMI or tenure may change |

| Repo-linked or benchmark-linked | Linked to an external benchmark | Rate movement may affect the loan faster |

| MCLR-linked | Linked to the bank’s internal benchmark | Reset timing becomes important |

A fixed rate may offer stability, but it may not always remain fixed for the entire loan tenure unless the loan terms clearly say so.

A floating-rate loan may initially appear cheaper, but the borrower must be comfortable with future movement.

The most important buyer question is:

Can my family manage the EMI if the interest rate increases?

Buyers should read the reset conditions, spread, benchmark and conversion charges carefully before selecting a loan.

What should buyers check before taking a ₹50 lakh home loan?

The home-buying decision should be tested against more than one EMI calculation.

| Check | Why it matters |

| Monthly income | Shows whether the EMI is sustainable |

| Existing EMIs | Reduces monthly flexibility |

| Credit score | Influences approval and pricing |

| Down payment savings | Reduces borrowing |

| Stamp duty and registration budget | Usually separate from property price |

| Emergency fund | Protects during income disruption |

| Interest-rate buffer | Helps manage future rate increases |

| Property approval | Reduces legal and financing risk |

| RERA status | Important for under-construction properties |

| Maintenance cost | Adds to monthly housing expense |

A buyer should also review:

- builder credibility,

- possession timeline,

- location,

- commuting cost,

- construction quality,

- legal title,

- and resale potential.

Who can safely consider a ₹50 lakh home?

A ₹50 lakh home may be financially manageable when the buyer has:

- monthly income of approximately ₹80,000 to ₹1 lakh,

- at least ₹10 lakh for down payment,

- separate savings for registration and interiors,

- low existing EMIs,

- a good credit profile,

- stable employment or business income,

- and an emergency fund covering at least six months of expenses.

It may become risky when:

- the buyer uses all savings for the down payment,

- income is unstable,

- there are multiple existing loans,

- the buyer has no emergency fund,

- the EMI exceeds comfortable income limits,

- or the home is purchased only because the bank approved the loan.

How much emergency fund should remain after buying?

A buyer should ideally retain an emergency reserve even after paying the down payment and registration charges.

A six-month emergency fund can include:

- six months of EMI,

- household expenses,

- insurance premiums,

- school fees,

- medical needs,

- and essential bills.

For example, if the monthly family expense including EMI is ₹70,000, a six-month reserve may be around ₹4.2 lakh.

This amount should remain separate from money allocated for furniture or interiors.

Should a buyer make a higher down payment?

A higher down payment can reduce:

- loan amount,

- monthly EMI,

- total interest,

- and the risk of financial stress.

For example, if a buyer pays ₹15 lakh instead of ₹10 lakh, the loan reduces from ₹40 lakh to ₹35 lakh.

However, the buyer should not use every available rupee to reduce the loan.

A balanced strategy is better:

- pay a reasonable down payment,

- retain an emergency fund,

- avoid unnecessary interior overspending,

- and prepay the loan gradually when extra income becomes available.

Carpet Area view

For a ₹50 lakh home, the safest planning rule is simple:

Do not calculate affordability only on the property price. Calculate it on the total cash requirement, monthly EMI, future interest-rate risk and family comfort.

A buyer earning ₹80,000 to ₹1 lakh per month may be able to manage a ₹40 lakh home loan with an EMI close to ₹33,500.

But the same loan can become stressful when the buyer has:

- multiple EMIs,

- unstable income,

- high monthly expenses,

- no emergency savings,

- or future family obligations.

The best home is not the one with the highest loan approval.

The best home is the one that still allows the family to save, plan and live peacefully after paying the EMI.

Final view

A ₹50 lakh home can be affordable for many middle-class Indian buyers, but only when the full financial picture is considered.

The decision should include:

- salary,

- down payment,

- EMI,

- interest rate,

- loan tenure,

- credit score,

- existing debt,

- stamp duty,

- registration cost,

- emergency savings,

- and long-term family needs.

The practical answer is:

To buy a ₹50 lakh home with a ₹40 lakh loan, a buyer should ideally have monthly income of around ₹80,000 to ₹1 lakh, limited existing debt and savings beyond the down payment.

The smart buyer’s rule is clear:

Do not buy the maximum home the bank allows. Buy the home your family can comfortably afford.

Sources:-

- Bank of Baroda official home loan page

https://www.bankofbaroda.in/personal-banking/loans/home-loan - ICICI Bank official home loan page

https://www.icicibank.com/personal-banking/loans/home-loan - ET Wealth article on the hidden cost of a large home loan EMI

https://m.economictimes.com/wealth/borrow/is-your-home-loan-ruling-your-life-know-the-hidden-cost-of-a-big-emi/articleshow/132173543.cms - Economic Times report on MCLR revision and benchmark-linked lending rates

https://m.economictimes.com/wealth/borrow/hdfc-bank-revises-mclr-lending-interest-rates-for-loan-borrowers-check-updated-list-base-bplr-fd-rates/articleshow/132232665.cms

Disclaimer: EMI, salary requirements and repayment figures in this article are approximate and intended for general understanding. Actual loan eligibility, interest rate, EMI and borrowing conditions may vary by lender, borrower profile and property.

Leave a Reply