For most Indian families, buying a home without a loan is difficult. That is why EMI has become a normal part of property buying.

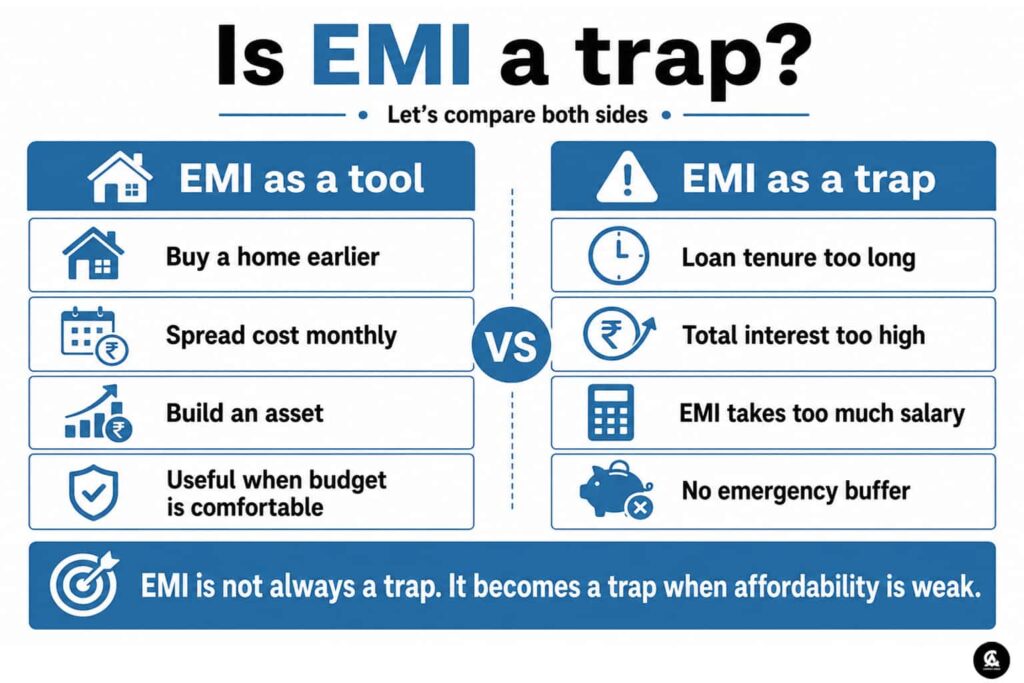

The problem is not EMI itself.

The problem starts when buyers look only at the monthly EMI and forget the full cost of the loan.

A home loan can help a family buy a house earlier, build an asset and avoid years of waiting. But the same home loan can become stressful if the buyer stretches the budget, chooses a very long tenure only to reduce the monthly EMI, ignores the total interest cost and assumes that future income will always keep rising.

So the real question is not whether EMI is good or bad.

The real question is: are you using EMI as a tool or falling into an EMI trap?

Why does EMI feel affordable at first?

EMI is designed to make a big purchase look manageable.

A ₹60 lakh or ₹80 lakh home may look impossible when seen as one large number. But when the same cost is converted into a monthly payment, the decision feels easier. This is why many buyers focus only on one question: “Can I pay this EMI every month?”

That question is important, but it is incomplete.

A smart homebuyer should also ask:

How much total interest will I pay?

How long will this loan continue?

How much of my salary will go into EMI?

Will I still have money for savings, insurance, children’s education and emergencies?

Can I handle the EMI if income is delayed or expenses rise?

When these questions are ignored, EMI slowly becomes a trap.

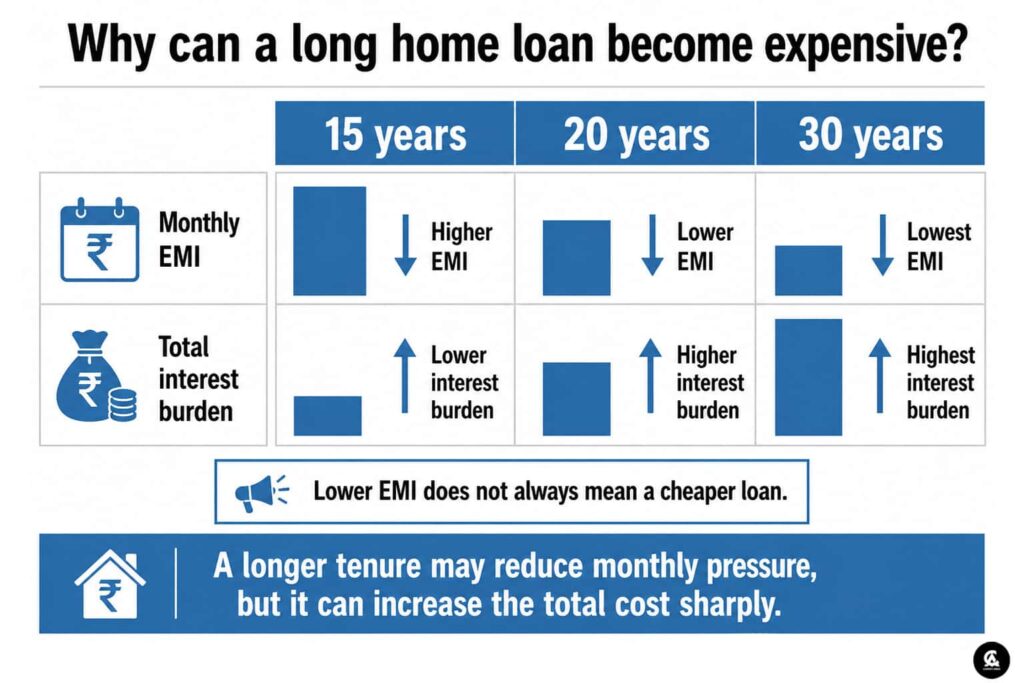

Why can a long home loan become expensive?

A longer home loan tenure reduces the monthly EMI, but it can increase the total interest burden sharply.

This is the biggest hidden cost many buyers miss. A 25-year or 30-year loan may look comfortable because the monthly EMI is lower, but the borrower may end up paying a very large amount as interest over the full tenure.

A recent Economic Times article explained this issue through the warning around 30-year home loans. It pointed out that in the initial years of a long home loan, a major part of the EMI often goes towards interest instead of principal repayment. That means the loan balance reduces slowly in the beginning, even though the borrower keeps paying every month.

This does not mean a long-tenure loan is always wrong. It may help some buyers manage cash flow. But buyers should understand one thing clearly: lower EMI does not always mean cheaper loan.

When does EMI become a trap?

EMI becomes a trap when it controls your life instead of supporting your plan.

This usually happens in four situations.

First, when the buyer takes the maximum loan possible only because the bank is willing to give it.

Second, when the buyer chooses a very long tenure without understanding the total interest cost.

Third, when the buyer has multiple EMIs at the same time, such as home loan, car loan, consumer loan and credit card dues.

Fourth, when the buyer has no emergency fund and still commits to a large home loan.

This is where the middle-class risk becomes real. A family may look financially comfortable on paper, but if most of the monthly income is already committed to EMIs, there is very little flexibility left.

A higher salary does not always mean financial freedom if the EMI burden rises with every income increase.

What about no-cost EMI?

The EMI trap is not limited to home loans.

No-cost EMI offers have also changed how people spend. A phone, furniture, appliance or gadget may feel affordable because the cost is divided into small monthly payments. But if the product price is inflated or the buyer loses a cash discount, the cost is not really zero.

Recent reporting has raised concerns that no-cost EMI can push buyers into purchases they may otherwise avoid. Hidden costs may come through higher product pricing, processing charges or loss of discounts.

For property buyers, the lesson is simple.

If EMI makes you buy something useful and affordable, it is a tool.

If EMI makes you buy something beyond your real capacity, it becomes a trap.

How much EMI is safe?

There is no one perfect number for every family, but the EMI-to-income ratio is very important.

Affordability is not only about property price. It also depends on income, interest rate and loan burden. A lower interest rate can improve affordability, but an overpriced property or very large loan can still make the EMI uncomfortable.

For a practical buyer, the safer approach is to avoid pushing EMI to the extreme limit. If the EMI takes too much of monthly income, the buyer may own a home but lose peace of mind.

A home should improve life, not make every month financially tight.

What happens if home loan EMI is not paid?

This is the serious side of EMI that many buyers do not think about during booking.

A home loan is not a casual promise. It is a legal and financial commitment. If EMIs are missed for a long period, the matter can become serious.

If a borrower does not pay home loan EMIs for a long time, the loan can be classified as a Non-Performing Asset. After that, the lender can begin recovery steps under the legal process, including notices and possible possession or auction if dues are not cleared.

This does not mean the bank auctions the home immediately after one missed EMI. There is a process. But it does mean buyers should never treat EMI default lightly.

If repayment becomes difficult, the borrower should speak to the bank early and explore options instead of ignoring calls and notices.

What should homebuyers check before taking a loan?

Before taking a home loan, buyers should not only check the property. They should also check their own financial strength.

Ask these questions before booking:

Is the EMI comfortable after monthly household expenses?

Do I have an emergency fund?

Will I still be able to save after paying EMI?

What is the total interest payable over the loan tenure?

Can I make part-prepayments in the future?

Is the property legally clear and RERA registered?

Is the builder reliable?

Is the total cost clear, including stamp duty, registration, GST, parking, maintenance, interiors and moving cost?

If the answer is unclear, the buyer should slow down.

How can buyers avoid the EMI trap?

The first rule is simple: do not buy only because the EMI looks manageable.

Look at the full loan cost.

A buyer can reduce risk by choosing a property within budget, keeping EMI at a comfortable level, maintaining an emergency fund, avoiding unnecessary consumer EMIs and making part-prepayments when possible.

If income increases in the future, the buyer can also consider increasing EMI or making occasional principal payments, depending on bank terms and personal financial planning.

The goal should be to own the home without becoming financially trapped by the home.

Final view

EMI is not the enemy.

For many Indian families, EMI is the bridge between renting and owning. It allows people to buy a home, create stability and build a long-term asset.

But EMI becomes dangerous when buyers confuse monthly affordability with real affordability.

A low EMI can hide a long tenure.

A long tenure can hide a huge interest cost.

A big home loan can hide years of financial pressure.

For Carpet Area readers, the message is clear.

Do not ask only, “How much EMI will I pay?”

Ask, “How much freedom will I still have after paying this EMI?”

A good home loan should help you buy a home.

It should not quietly take away your financial peace.

Sources:-

Times of India:

Economic Times Realty:

https://realty.economictimes.indiatimes.com/news/residential/lower-home-loan-rates-improve-housing-affordability-across-most-cities-in-2025-knight-frank/126270365

Leave a Reply