India’s retail real estate story is changing fast. For years, the conversation around retail property was mostly about online shopping, weak footfall, and whether malls could survive the digital shift. But the 2025 leasing numbers tell a very different story. Physical retail is not disappearing. In fact, the strongest locations are becoming more valuable, more competitive, and more important for brands that want visibility, footfall and premium customers.

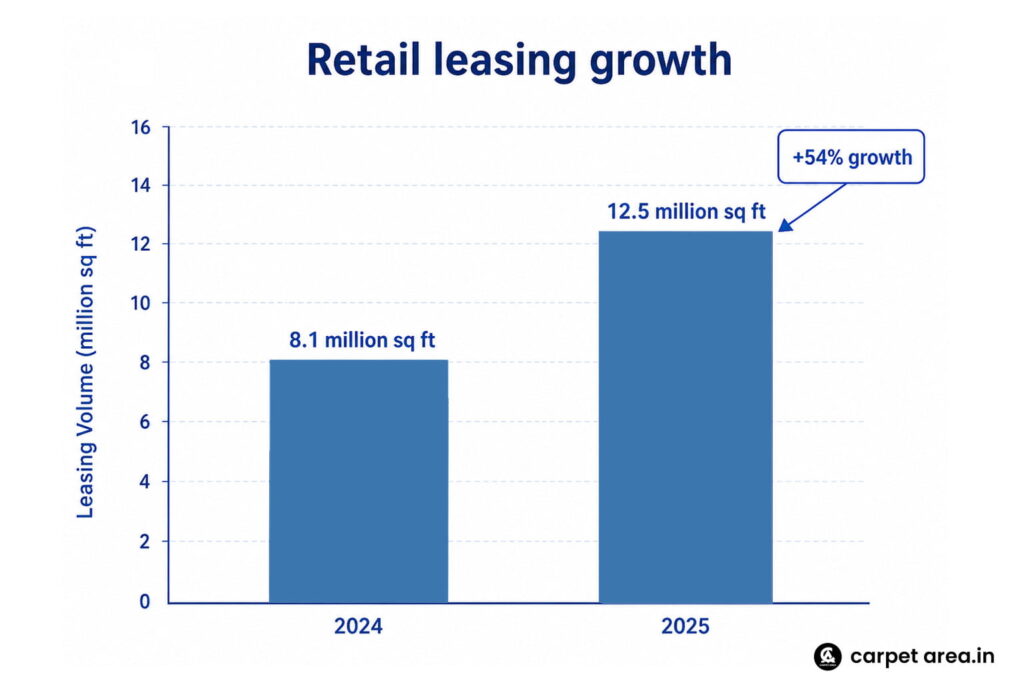

The biggest signal comes from retail leasing. Across India’s top seven cities, gross retail leasing across malls, high streets and prime retail developments increased from 8.1 million sq ft in 2024 to 12.5 million sq ft in 2025. That means leasing activity grew by around 54% in one year, taking the market to a three-year high. This is not a small recovery. It shows that brands are again willing to take physical space, but they are being very selective about where they go.

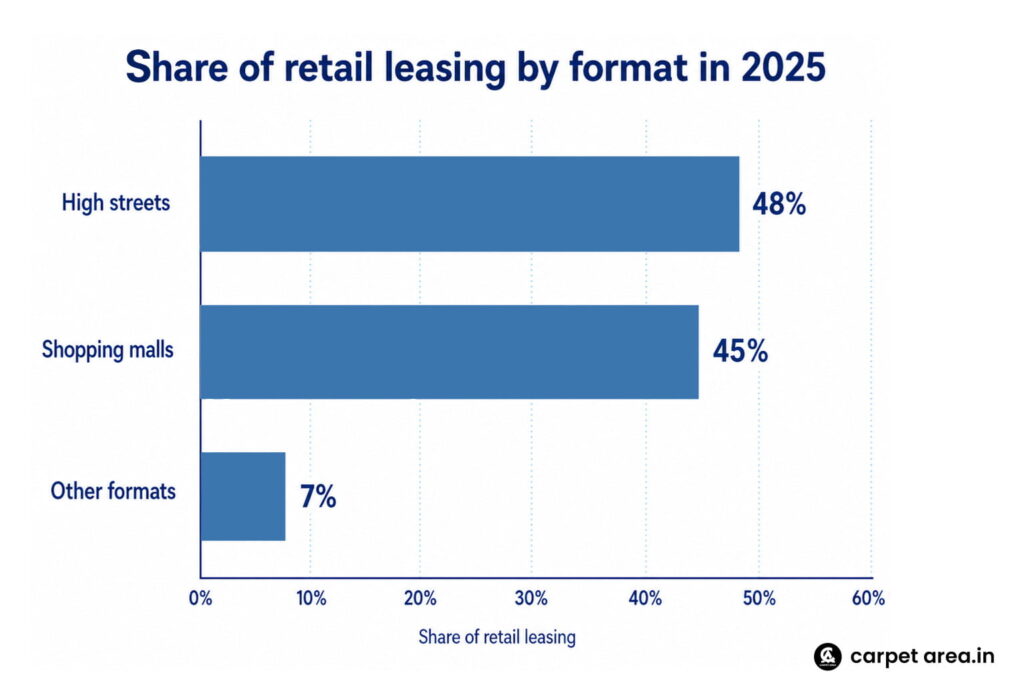

What makes this trend interesting is that the demand is not spread equally across every retail property. The winners are clear: high streets and quality malls. JLL data shows that high streets accounted for 48% of total retail leasing activity in 2025, while shopping malls contributed 45%. Together, these two formats captured 93% of the leasing market, leaving only 7% for other retail formats. That tells us one simple thing: brands are not just looking for space. They are looking for locations that can bring customers, visibility and stronger sales potential

High streets are winning because they offer something that many enclosed retail formats cannot always provide: easy access, everyday visibility and strong neighbourhood-level movement. A good high street is not dependent only on weekend footfall. It gets office workers, residents, students, commuters, shoppers and diners throughout the week. For brands in fashion, jewellery, electronics, food, beauty, wellness and lifestyle, that kind of daily movement is extremely valuable.

Grade-A malls are winning for a different reason. They offer scale, parking, security, better tenant mix, food courts, entertainment and a controlled shopping environment. When a mall is well located and professionally managed, it becomes more than a shopping destination. It becomes a full-day consumption space. Families go there for shopping, movies, restaurants, gaming, cafes, salons and events. That is why good malls continue to attract strong brands even when weaker malls struggle.

The city-wise numbers also show where the strongest action is happening. In 2025, Delhi-NCR led retail leasing with 3.02 million sq ft, followed by Bengaluru with 2.97 million sq ft, Hyderabad with 2.91 million sq ft, and Mumbai with 2.1 million sq ft. These four markets alone show how concentrated the demand has become in large urban consumption hubs. Delhi-NCR, Bengaluru and Hyderabad were especially strong, supported by income growth, new supply, expanding brands and stronger consumer spending.

For investors and developers, this is an important signal. The market is not saying that every retail property will perform well. It is saying that the best-located retail assets are becoming stronger. A poorly located mall with weak tenant mix may still struggle. A badly planned retail complex may still face vacancy. But a strong high street or Grade-A mall in the right micro-market can become a powerful income-generating asset.

This also explains why rental returns are becoming an important part of the story. Prime high streets are seeing strong interest because brands want street-facing visibility and direct customer access. In markets like Khan Market, where rents have been reported around Rs 1,600 per sq ft, the value of premium high-street frontage becomes very clear. Such locations are not just retail addresses. They are brand statements. A store in a premium high street can work like advertising, customer acquisition and sales infrastructure all at once.

The rise of high streets also reflects how Indian consumers shop today. People may discover products online, compare prices on their phone and still visit a store before buying. For categories like fashion, jewellery, electronics, fitness, food, beauty and lifestyle, the physical experience still matters. Customers want to touch, try, taste, compare and trust. That is why offline retail is not dead. It is becoming more experience-driven.

Grade-A malls benefit from the same shift. A modern mall is no longer only about shopping bags. It is about experience. People visit for cafes, gyms, cinemas, kids’ zones, restaurants, salons, pop-up events and lifestyle spending. This gives mall owners more ways to generate footfall and gives brands a stronger reason to lease space in well-managed centres.

There is another reason this trend matters. India still does not have enough high-quality organised retail space compared with the size of its consumer market. As more global and domestic brands expand, the pressure on good retail locations is likely to remain strong. That shortage of quality space can support rentals in the best assets, especially in micro-markets where demand is high and supply is limited.

For home buyers, this trend also matters indirectly. Strong retail hubs often improve the attractiveness of nearby residential areas. When a neighbourhood gets better shopping, dining, fitness, entertainment and daily convenience options, the lifestyle value of that location improves. This does not mean prices will automatically rise everywhere, but it does mean that good retail infrastructure can become a positive factor in how people judge a location.

For NRI and HNI investors, the message is even clearer. Retail real estate should not be judged only by the size of the building. It should be judged by location quality, tenant mix, frontage, footfall, brand demand, parking, catchment income and long-term leasing strength. A smaller high-street asset in the right location can sometimes be more attractive than a larger but weaker retail property.

The larger takeaway is simple: India’s retail real estate market is becoming more selective. The total leasing number, from 8.1 million sq ft in 2024 to 12.5 million sq ft in 2025, shows growth. The 54% rise shows momentum. The 48% share of high streets and 45% share of malls shows where the demand is going. And the city-wise figures show that Delhi-NCR, Bengaluru, Hyderabad and Mumbai are leading the next phase of organised retail expansion.

High streets and Grade-A malls are becoming retail real estate’s big winners because they offer what brands need most today: visibility, quality footfall, consumer trust and a strong offline experience. In a market where average retail space may still face challenges, premium retail locations are quietly becoming some of India’s most important commercial real estate assets.

There is also a supply-side reason why grade-A malls matter so much. India still does not have enough top-quality retail space in the best categories. Reuters reported in March that India has only three true luxury malls at present and that even premium brands ready to enter the country face what market participants described as zero availability in some top locations. More broadly, Reuters cited Anarock data showing India has about 110 million sq ft of grade-A mall stock, far below China and the United States. This shortage is important because it means quality malls are not competing in an oversupplied environment. In many cases, they are operating in a supply-constrained market where brand demand still exceeds availability. That naturally supports rental resilience.

This shortage of quality space also explains why the market now seems more selective rather than broadly bullish. Not every mall is winning. Not every high street is premium. The strength is concentrated in the best locations and best assets. That is a healthy sign because it suggests retailers are becoming more disciplined. They are not expanding blindly. They are choosing carefully. Anarock’s Releap 2026, as cited by Mint and other coverage, suggests that retailers are focusing more on targeted expansion, mid-sized stores, and higher-quality visibility-led locations. That makes the current retail-property recovery more credible than a simple post-pandemic bounce. It is not just more activity. It is better-filtered activity.

For investors, this creates a more interesting decision framework than before. High streets offer the possibility of stronger rent appreciation and long-term scarcity value, but they can also be operationally messier and more location-sensitive. Grade-A malls offer more stable cash flows, structured leasing environments, and better institutional comfort, but they may not always deliver the same headline rent spikes as a truly iconic street location. That means the question is no longer whether retail real estate is attractive at all. The more useful question is which type of retail asset fits the investor’s risk appetite and return expectations better. ET Wealth’s framing captures this well: high streets can still generate premium rental returns, while top malls offer steadier performance.

For cities, there is a wider lesson here too. Strong high streets and strong malls do not just create value for landlords. They shape neighborhoods, transport patterns, employment, local services, and even residential desirability. A vibrant retail corridor usually spills into the surrounding economy. This is one reason retail demand is being watched more seriously again. It is not just about stores opening or rents moving up. It is about whether a city’s best commercial zones are strengthening as everyday urban destinations. When that happens, retail real estate becomes part of the city-growth story, not just a narrow investment story.

In the end, the commercial rental-return story is really about one big idea: quality still wins. India’s best high streets are winning because brands cannot easily replace their visibility and consumer pull. India’s best grade-A malls are winning because organized, well-run, supply-constrained assets still attract serious tenants and capital. The result is a retail market that is no longer easy to dismiss as old economy real estate. It is evolving into a more selective, more mature, and more strategically valuable segment of commercial property. That is why this story deserves attention. In India’s big-city retail market, the strongest spaces are not getting cheaper or easier to find. They are becoming more important.

Leave a Reply