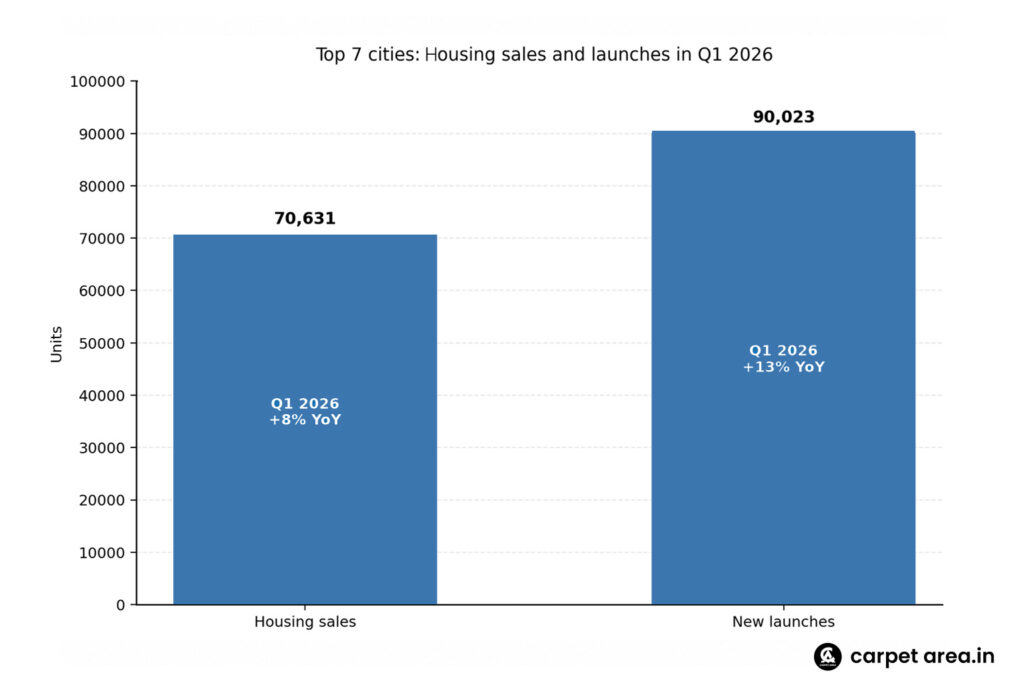

India’s housing market has entered a phase that looks positive on the surface but more complicated once you look deeper. Sales are still rising, new launches are still coming, and the sector is clearly not in retreat. But the rhythm of the market is changing. The latest JLL-based data shows housing sales across India’s top seven cities rose 8 percent year on year to 70,631 units in Q1 2026, while new apartment launches grew faster at 13 percent to 90,023 units. That gap matters because it tells us something important: demand is still alive, but buyers are no longer responding with the same speed or confidence across the board.

That is why this story deserves more than a simple “sales are up” interpretation. If sales rise while launches rise even faster, the message is not straightforward optimism. It suggests that developers remain willing to bring new supply to market, but buyers are taking more time, making more comparisons, and choosing more carefully. JLL described this as a temporary softening in buyer sentiment rather than a structural weakness, and that distinction matters. A cautious market is very different from a broken one. In this case, the data suggests that India’s residential sector is adjusting, not collapsing.

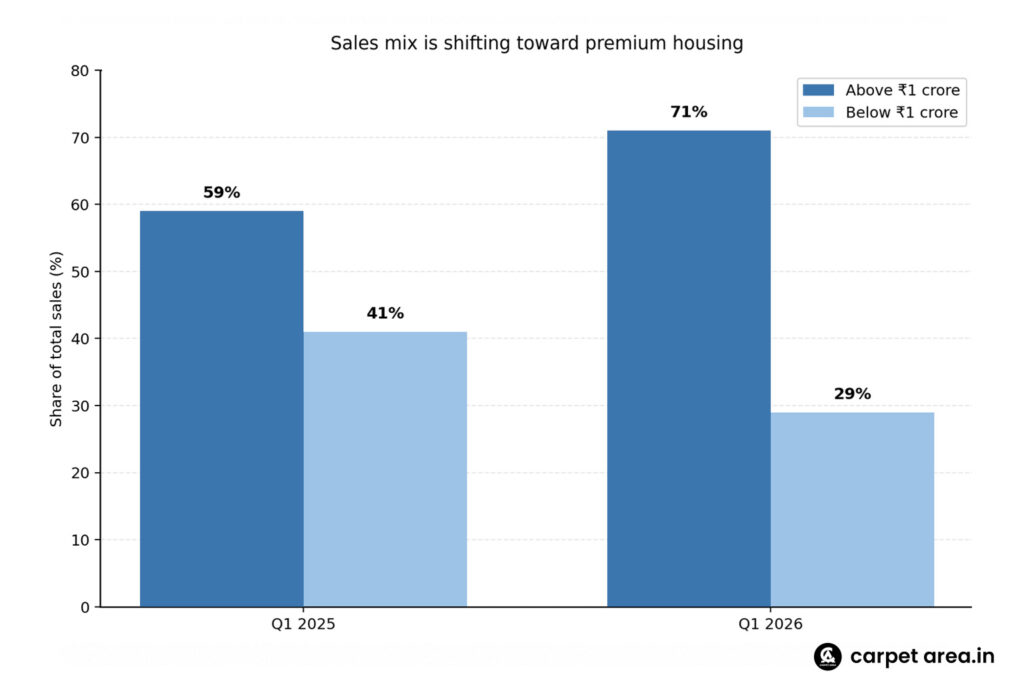

One of the clearest signs of this transition is where the demand is now concentrating. According to the report cited by Hindustan Times, homes priced above ₹1 crore accounted for 71 percent of total sales in Q1 2026, up from 59 percent a year earlier. This segment registered 30 percent annual growth, and the ₹1.5 crore to ₹3 crore band led with an exceptional 67 percent year-on-year increase. At the same time, the sub-₹1 crore segment shrank 24 percent, with its market share falling to 29 percent from 41 percent. That is not a small shift. It shows that India’s housing growth is becoming much more premium-led than before.

This is where the story becomes especially meaningful for ordinary buyers. A rising market normally sounds encouraging, but not every part of the market rises in the same way. If more of the growth is happening above ₹1 crore and less in the under-₹1 crore segment, then a large part of the country’s housing demand may be getting pushed upward by price pressure rather than moving upward by choice. In simple terms, many buyers may still want homes, but fewer of them are finding what they can comfortably afford in the lower-ticket segment. That appears to be one of the clearest undercurrents in this report. This is an inference drawn from the sharp divergence between premium and sub-₹1 crore demand.

The price environment explains a lot of this. Apartment prices rose 8 percent to 20 percent across the seven major cities in the January to March period, according to the same report. JLL attributed this to higher input costs, and the report also suggested prices may continue appreciating, though at a slower pace. This matters because when prices rise too quickly, the market naturally becomes more selective. Buyers start weighing location, credibility, and value more carefully. The result is not necessarily a drop in demand, but a narrowing of demand into the segments and projects where buyers still feel comfortable committing.

Another important detail in the report is that demand remains concentrated in a handful of major cities. Bengaluru, Mumbai, Pune, and Delhi-NCR, each with more than 10,000 unit sales, together accounted for around 77 percent of total demand in Q1 2026. That tells us two things. First, the market is still being driven by the biggest urban centres. Second, the headline national growth number is heavily dependent on the strength of a few cities rather than evenly spread demand everywhere. This makes the market look resilient, but also more selective geographically.

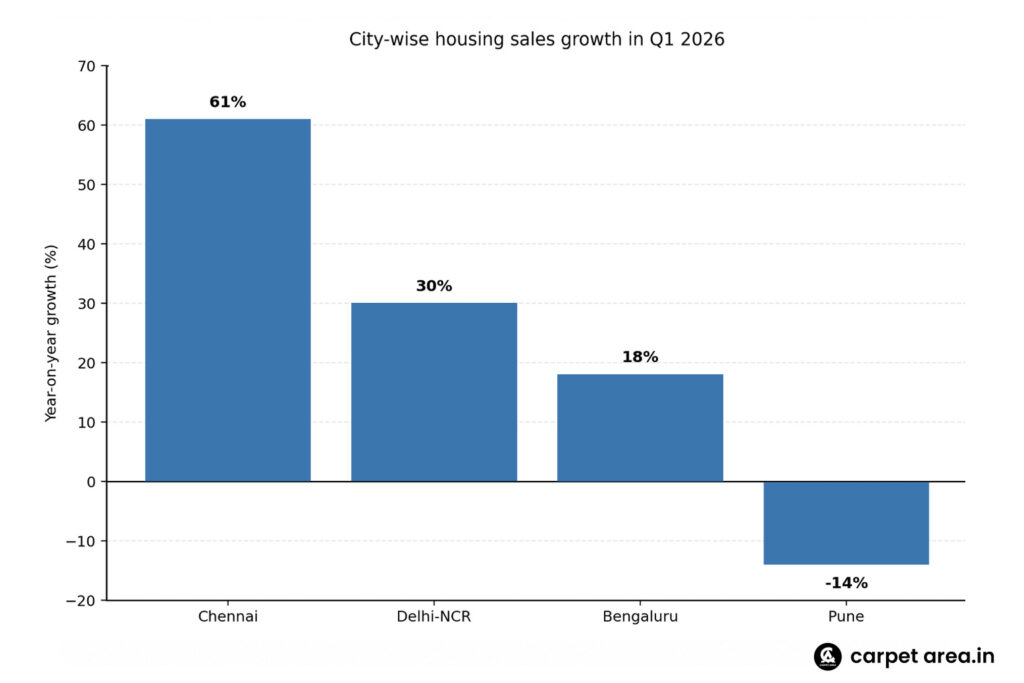

The city-level divergence is another reason this is such a useful market story. Chennai reportedly led with a 61 percent surge in sales, followed by Delhi-NCR at 30 percent and Bengaluru at 18 percent, while Pune saw a 14 percent decline amid lower launches. That tells us India’s residential market is not moving in one smooth national line. Different cities are responding differently based on supply, local affordability, buyer profile, and market momentum. So when people talk about the housing market as if it is a single story, they often miss the fact that it is really several city stories moving at different speeds.

The launch side of the story is just as important. New supply rose to 90,023 units, a 13 percent year-on-year increase and a 32 percent quarter-on-quarter jump. Bengaluru led with 27,055 launches, up 32 percent year on year, while Delhi-NCR saw 64 percent growth in launches and accounted for 45 percent of total quarterly launches. Those are strong supply numbers, and they show that developers are not behaving like a sector under stress. They are still putting product into the market in a significant way. That makes the sales-launch gap even more interesting, because it reinforces the idea that the market’s current issue is not confidence among developers. It is measured confidence among buyers.

For developers, this is a market that still offers opportunity, but not the kind of easy momentum that can carry every project. In a phase like this, launches alone are not enough. Product positioning matters more. So do brand trust, pricing discipline, project quality, and alignment with real buyer budgets. The fact that supply is growing faster than demand suggests that the market is becoming less forgiving. Projects that are well located and properly priced may continue to do well. Others may find buyers more hesitant than before. This is an inference supported by the divergence between launches and sales and by JLL’s observation that buyers are exercising greater discretion amid economic uncertainty.

For homebuyers, the current phase may actually be more useful than it first appears. A market that is still active but no longer blindly aggressive often creates a better decision window. Buyers can compare more carefully, negotiate more intelligently, and pay closer attention to long-term livability rather than only short-term appreciation. At the same time, the shift toward premium housing is a reminder that affordability pressure has not gone away. In many cities, it may actually be worsening. So while the overall market remains healthy, the pressure on entry-level and mid-budget buyers is still very real.

What makes this story especially important for CarpetArea readers is that it captures a market in transition, not in crisis. India’s housing demand is still growing. That is the headline truth. But the deeper truth is that buyers are getting more selective, premium housing is taking a larger share of activity, and supply is rising faster than actual absorption. That combination usually signals a maturing market. It means the easy phase of broad-based buying is giving way to a more filtered phase where quality, affordability, and confidence do not move together automatically. This interpretation is grounded in the reported growth rates, segment shifts, and city-wise divergence.

In the end, the real takeaway is not that India’s housing market is strong or weak. It is that it is becoming more selective. Demand is still present, but it is choosing more carefully. Developers are still launching, but they may need sharper alignment with what buyers can absorb. Premium housing is still growing fast, but the shrinking sub-₹1 crore market shows why affordability remains a serious pressure point. That is why this is a valuable story right now. It does not just say where the market is. It shows where it may be heading next.

Leave a Reply