When land deals fall, the first reaction is usually simple: the market must be slowing down. But India’s FY26 land acquisition data tells a more layered story. Yes, the number of land deals has dropped. But at the same time, large listed real estate developers are increasing their control over the market. That means the real story is not just slowdown. It is consolidation.

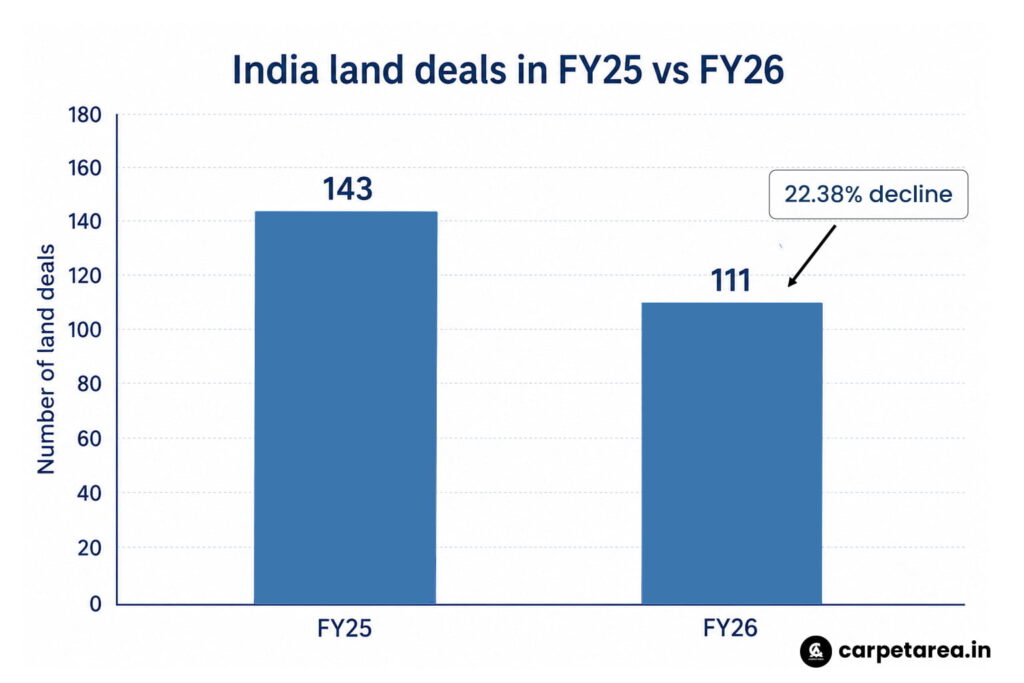

According to Anarock data reported by ET Realty, India recorded 111 land deals covering around 2,994 acres in FY26. This was lower than 143 deals in FY25, which means land deal activity declined by about 22.38%. On the surface, this looks like a clear fall in developer appetite. But once we look deeper, the picture changes.

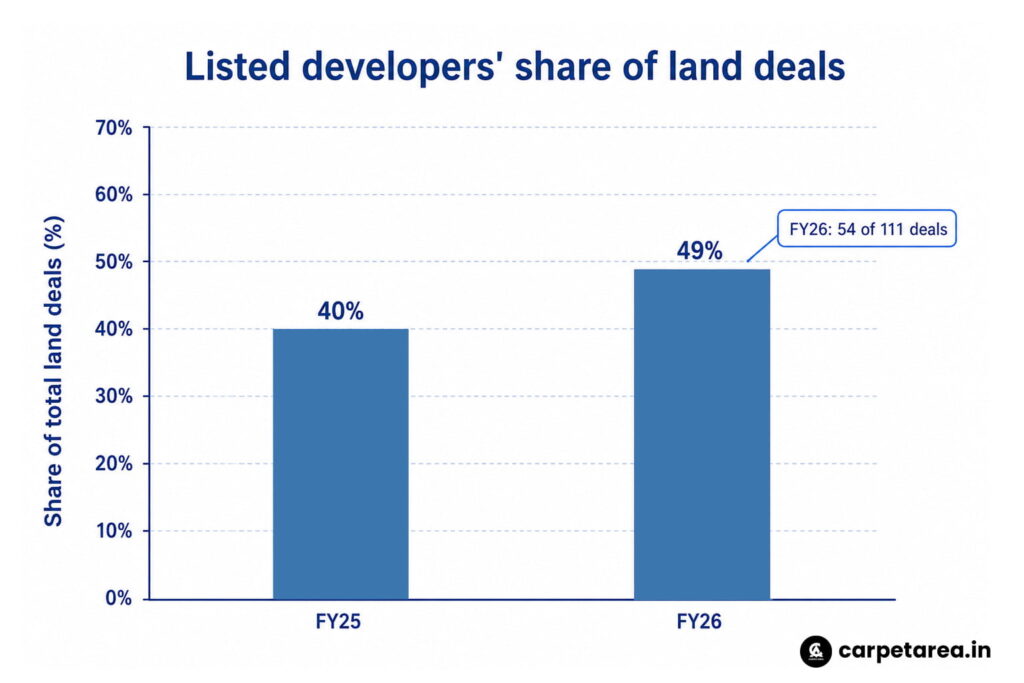

The important part is who is buying land. Listed real estate developers accounted for 54 of the 111 land deals in FY26. These deals covered more than 1,433 acres, giving listed developers around 49% share of total transactions and around 48% share of the total land area transacted. In simple words, almost every second land deal was done by a listed developer.

This is why the dip in land deals should not be read as a collapse in demand. It looks more like a market where smaller players are becoming cautious, while large developers are still buying strategically. Land acquisition has become expensive, approval-heavy and more closely linked with long-term funding capacity. In such a market, developers with cleaner balance sheets, stronger brand value and better access to capital naturally get an advantage.

The shift becomes clearer when we compare the share of listed developers over time. In FY25, listed developers accounted for around 40% of all land deals. In FY26, their share rose to 49%. This increase happened even though total deals fell from 143 to 111. That means large developers did not simply benefit from a growing market. They gained share in a more selective market.

For homebuyers, this matters because land today becomes housing supply tomorrow. When listed and Grade-A developers buy more land, future launches may increasingly come from organised players. Anarock’s analysis also showed that listed and Grade-A developers together accounted for about 45% of new housing supply across the top seven cities in FY26, slightly higher than 43% in FY25. In NCR, their share of new supply was much higher at around 66%.

This points to a bigger “flight to trust” in Indian real estate. Buyers are more aware now. They check RERA status, possession records, brand reputation, construction progress and developer financial strength. After years of delayed projects in many markets, especially in NCR, buyers are increasingly giving preference to developers who look more reliable. This is one reason listed and Grade-A developers are becoming stronger.

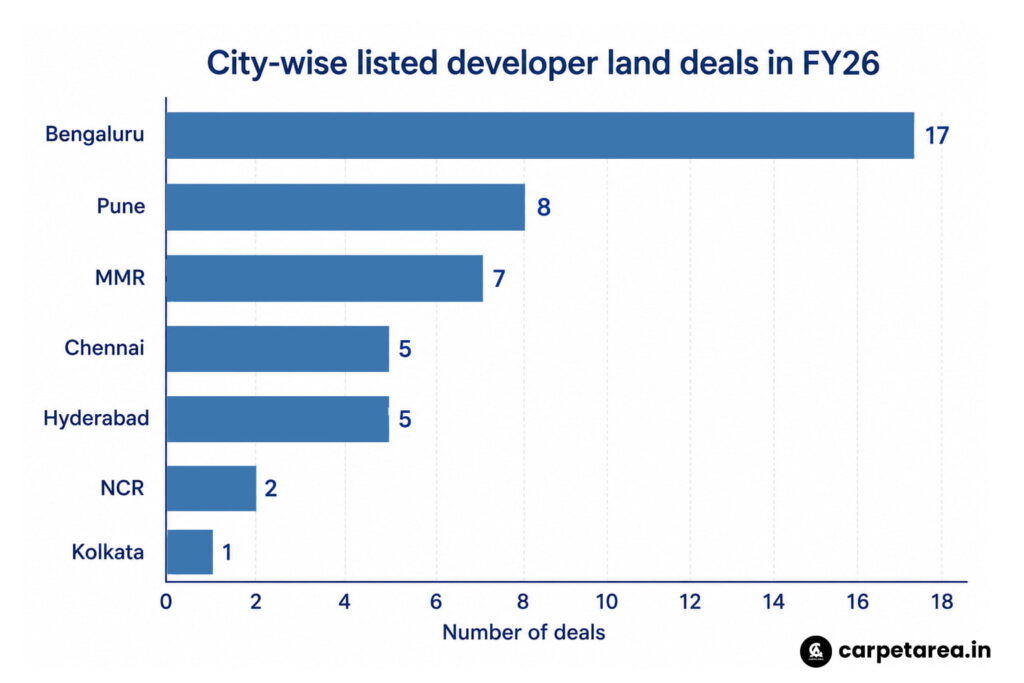

The city-wise data also tells an interesting story. Bengaluru emerged as the top market for listed-player land acquisitions, with 17 deals covering more than 293 acres. Pune recorded 8 deals covering around 78 acres, while MMR saw 7 deals covering more than 51 acres. Chennai and Hyderabad each saw 5 deals, while NCR recorded only 2 deals in Gurugram and Kolkata saw 1 deal.

Leave a Reply