India’s real estate market has had a strong run over the past few years. Housing demand improved, premium homes sold faster, office leasing stayed active, and developers became more confident about new launches. But the latest Knight Frank-NAREDCO Real Estate Sentiment Index shows that the mood of the market is now changing. The sector is not collapsing, but it is clearly becoming more careful.

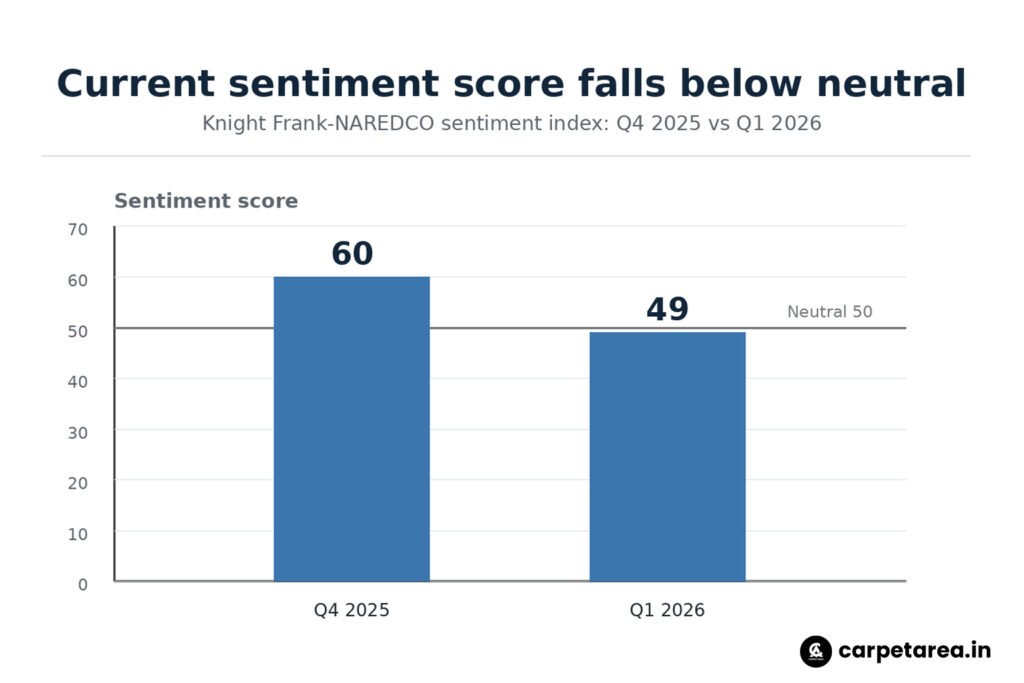

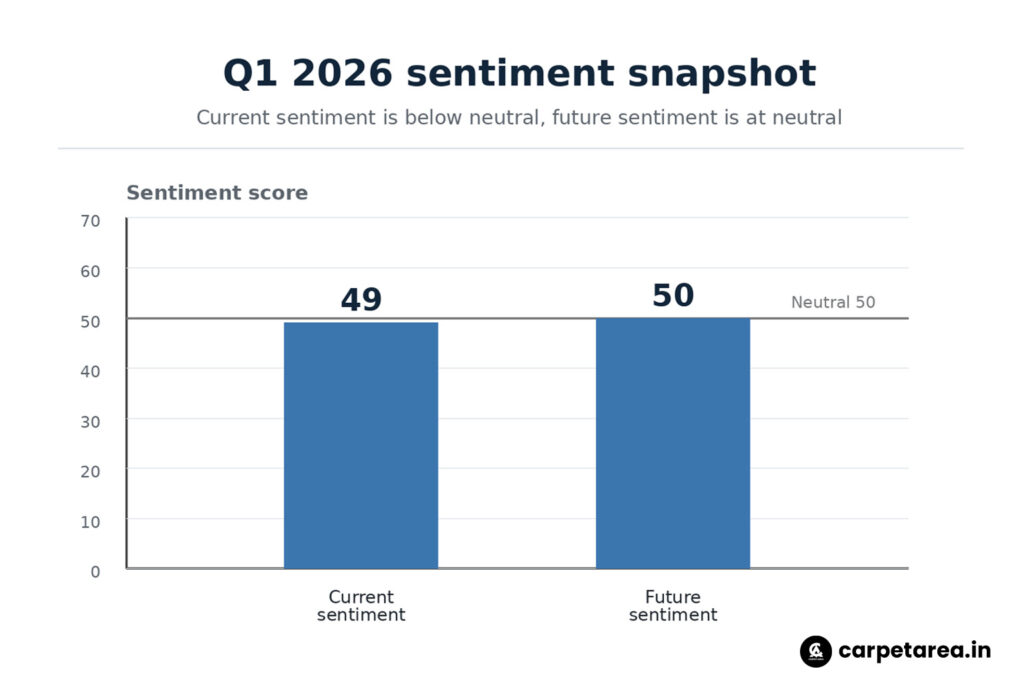

According to the Q1 2026 Real Estate Sentiment Index, the Current Sentiment Score fell sharply from 60 in Q4 2025 to 49 in Q1 2026. This is important because the index uses 50 as the neutral mark. A score above 50 shows optimism, 50 shows neutral sentiment, and below 50 shows pessimism. So when the current score falls to 49, it means stakeholders are becoming more cautious about the present market environment.

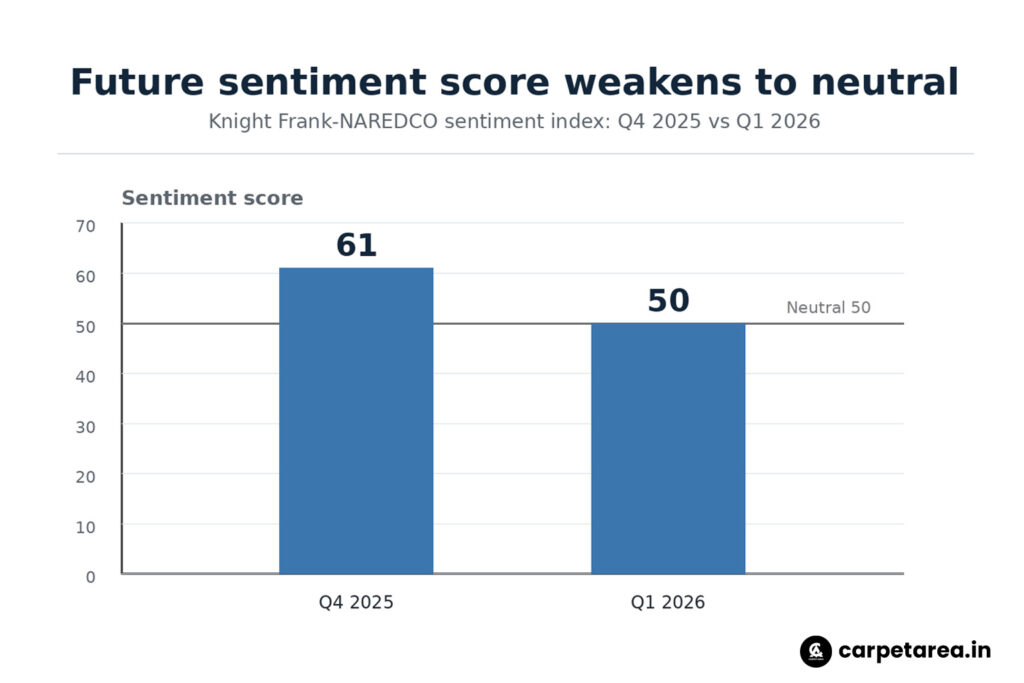

The future outlook has also softened. The Future Sentiment Score declined from 61 in Q4 2025 to 50 in Q1 2026. This does not mean developers and investors have turned negative about the long-term future of Indian real estate. But it does show that they are no longer looking at the next few months with the same level of confidence that they had earlier. The market has entered what the report calls a phase of cautious recalibration.

The word “recalibration” is important. It means the market is adjusting itself after a strong growth cycle. In simple terms, developers may become more selective about launches, investors may become more careful about valuations, lenders may become stricter about project funding, and buyers may take more time before committing to a property purchase.

The biggest reason behind this change is global uncertainty. The report points to global macroeconomic volatility, elevated crude oil prices, inflationary pressure, construction and logistics cost increases, and tighter financial conditions as factors weighing on sentiment. Even though India’s domestic economic fundamentals remain stable, global risks are now influencing real estate demand, supply and project viability.

For homebuyers, this matters because cost pressure can affect both prices and timelines. When crude oil prices rise, many construction-linked items become more expensive. Transport, logistics, building materials and finishing costs can all come under pressure. Developers may then either increase prices, delay launches, revise project phasing or become more cautious with new commitments.

This does not mean prices will automatically fall. In fact, in many good locations, prices may remain firm because land costs, construction costs and finance costs are still high. A cautious market does not always mean a cheaper market. Sometimes it means fewer impulsive launches, slower decision-making and more focus on quality demand.

The residential segment is showing signs of moderation after a strong run. Reports based on the index say housing sales and new launches moderated in Q1 2026, reflecting cyclical consolidation and cautious buyer sentiment. The report also says demand may soften further in the near term, while prices may remain firm or continue rising in some pockets.

This is an important signal for buyers. During a booming market, many buyers rush because they fear prices will move up quickly. In a cautious market, buyers get more time to compare projects, check RERA details, study possession timelines, negotiate better and avoid weak projects. The advantage shifts slightly from urgency to due diligence.

For developers, the message is different. They cannot assume that every launch will sell simply because the market was strong earlier. Buyers are becoming more selective. Projects with good location, trusted developers, realistic pricing, clear approvals and visible construction progress may continue to do well. But projects with weak access, poor pricing or unclear delivery confidence may face slower sales.

The office market appears more resilient than housing sentiment. Business Standard reported that office leasing activity reached a record high in Q1 2026 even as overall real estate sentiment softened. This shows that different parts of the real estate market are moving differently. Residential may be recalibrating, while office demand continues to benefit from occupier activity.

This is why investors should not read the index as a simple “good market” or “bad market” signal. It is more accurate to say that the market is becoming segmented. Some cities, corridors and asset classes may remain strong, while others may slow. Premium projects in strong micro-markets may still attract demand, while overpriced or poorly connected projects may struggle.

The regional trend also supports this selective view. Reports say sentiment softened across all regions. North and South slipped into pessimistic territory, while West remained relatively more resilient and stayed above the neutral mark despite some demand moderation. This means the market mood is not uniform across India.

For NRI and HRI investors, this cautious phase can actually be useful if approached carefully. Instead of chasing hype, investors can study markets more patiently. They should look at rental demand, infrastructure completion, developer credibility, resale liquidity, RERA status and actual end-user demand. In a cautious market, discipline matters more than excitement.

For homebuyers, the checklist should be simple. Check whether the project is registered under RERA. Compare carpet area and total cost. Look at construction progress. Study the possession date. Check whether similar ready properties are available nearby. Understand maintenance charges. Avoid booking only because of a launch discount or sales pressure.

The larger message from the Knight Frank-NAREDCO index is clear. India’s real estate market is still supported by long-term urbanisation, income growth, infrastructure spending and housing aspiration. But the short-term mood has become more careful because global and cost-related risks are rising. This is not panic. It is a pause for reassessment.

In simple words, the market is not saying that demand has vanished. It is saying that the easy growth phase may be slowing down. Developers, investors and buyers will now have to make sharper decisions. Strong projects will still find buyers. Weak projects will face more questions. And that is why this cautious recalibration phase may actually make the market healthier in the long run.

Leave a Reply