Affordable housing is one of the most important words in Indian real estate. It affects homebuyers, banks, developers, government schemes and policy incentives. But there is now a serious question: does the old definition of affordable housing still match today’s property prices?

This question has come back into focus after banks reportedly asked the government to review the definition of affordable housing. The concern is simple. Property values have risen, borrowing costs have increased, and home loan ticket sizes are much higher than before. Because of this, many homes that are still “affordable” for middle-income buyers may no longer fit into the technical affordable housing category.

The strongest signal came from SBI chairman C S Setty. He said SBI’s average home loan ticket size has gone up to around ₹51 lakh, compared with about ₹35 to ₹40 lakh two years ago. That jump is important because SBI is India’s largest lender and has a major presence in the home loan market. When the country’s biggest bank says the definition needs a review, the issue becomes much bigger than one bank’s internal data.

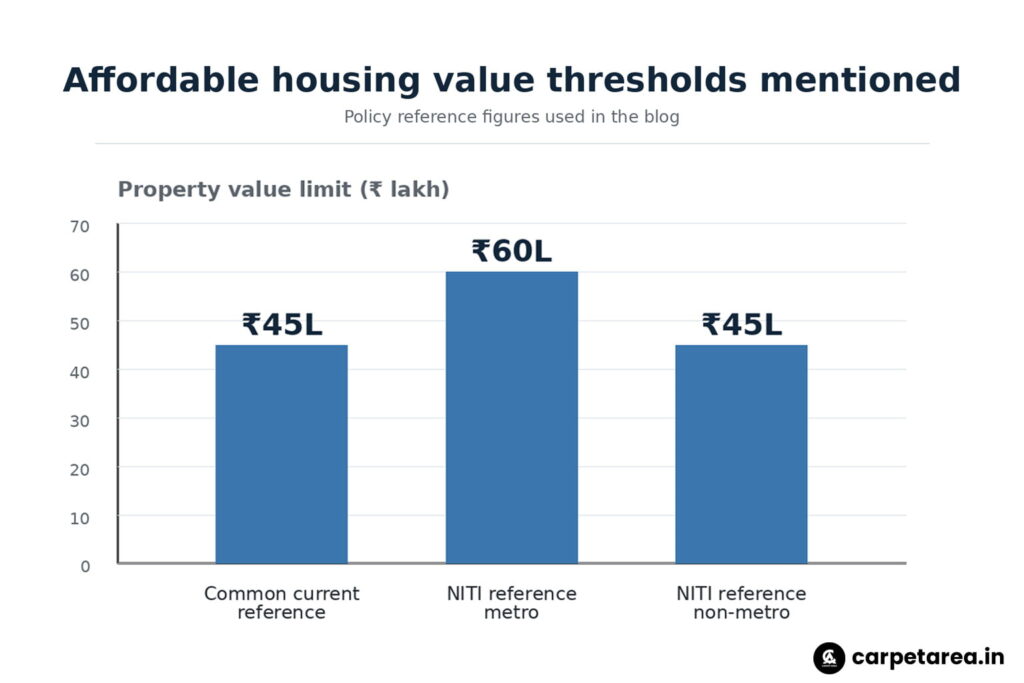

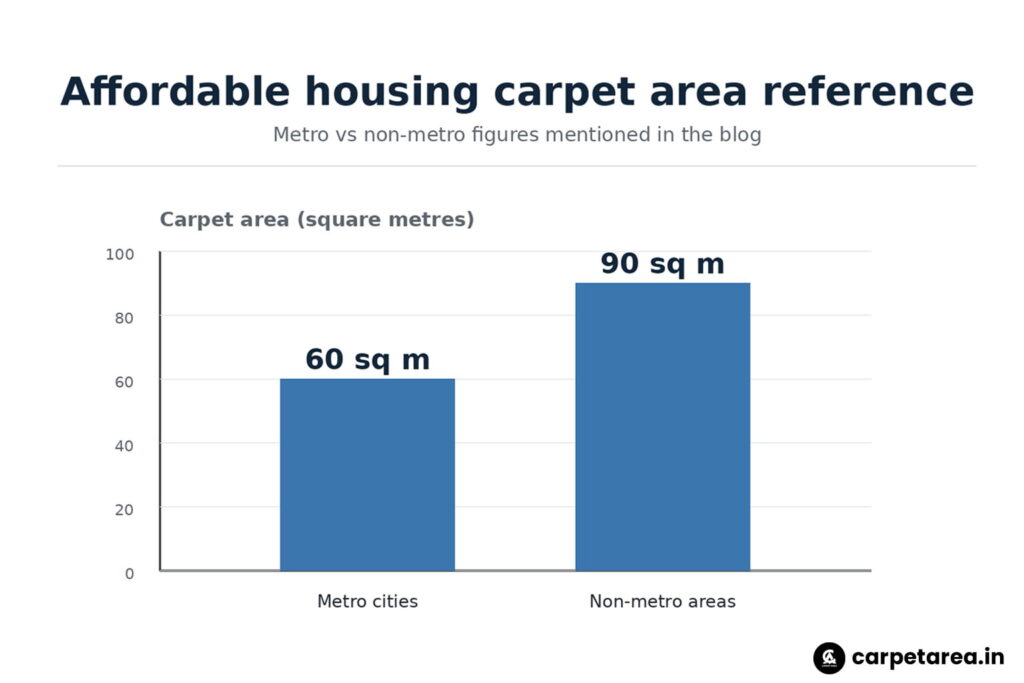

At present, affordable housing is often linked to property value and carpet area limits. Reports mention that a home is treated as affordable housing under certain policy contexts if its cost is up to ₹45 lakh and it meets specified carpet area norms. Business Today also reported that NITI Aayog’s December 2025 reference considered units with 60 square metres carpet area in metro cities and value not exceeding ₹60 lakh as affordable, while for non-metro areas, 90 square metres and value not exceeding ₹45 lakh were cited.

This shows the problem clearly. India does not have one simple affordability reality. A ₹45 lakh home may still be available in some smaller towns, but in many urban markets, that number may not buy a practical family-sized home in a decent location. In cities where land, construction cost, labour cost, taxes and financing cost have all increased, the old threshold can start looking disconnected from the market.

For homebuyers, this matters directly. If a property does not qualify as affordable housing under official norms, buyers may miss certain benefits, lenders may treat the loan differently, and developers may also have less incentive to create homes in that segment. Affordable housing is not just a label. It can influence priority sector lending treatment, tax benefits, policy support and product planning.

The bigger issue is that affordability is not only about the flat price. It is also about the total cost of ownership. A buyer today has to consider stamp duty, registration, GST where applicable, parking charges, floor-rise charges, maintenance deposit, club charges, loan processing fees and EMI burden. So even if the base price looks manageable, the final payable amount can move far above the old affordability limit.

Interest cost is another major factor. When home loan rates remain high or EMIs become heavier, affordability reduces even if the property price remains the same. A buyer who could comfortably afford a ₹40 lakh loan two years ago may now be looking at a higher EMI for a similar or slightly better property. That is why banks are asking for rising ticket sizes and interest costs to be considered while redefining the category.

For developers, an outdated affordable housing definition can create another problem. If official thresholds are too low compared with actual development costs, developers may find it difficult to build viable affordable projects in major cities. Land prices alone can make it hard to deliver homes within old value caps. This may push developers toward premium or mid-premium projects, where margins are better and pricing flexibility is higher.

This is already visible in many large cities. The supply of genuinely affordable homes in good locations is limited. Buyers either move farther from the city centre or compromise on size, connectivity or project quality. If the definition is updated realistically, developers may again find more reason to plan homes for the middle-income segment.

But redefining affordable housing must be done carefully. If the limits are raised too much, the benefit may shift away from lower and middle-income buyers and move toward higher-priced homes. The purpose of affordable housing should remain buyer protection and access to home ownership. It should not become a way to give incentives to projects that are not truly affordable for ordinary families.

The government will therefore need a balanced approach. It may have to consider city-wise price differences, carpet area, income levels, loan size, interest burden and actual market prices. A single national price limit may not work well because housing costs in Mumbai, Bengaluru, Gurugram, Lucknow, Indore and Jaipur are very different.

For homebuyers, the practical takeaway is clear. Do not judge affordability only by the brochure price. Check the all-inclusive cost, carpet area, EMI, loan tenure, interest outgo, location, travel cost and maintenance charges. A home is affordable only if the buyer can live in it comfortably without stretching household finances dangerously.

For investors, this debate also matters because affordable and mid-income housing are large demand segments. If the definition is revised sensibly, it could support fresh demand, improve loan eligibility and encourage more developers to serve the mass housing market. But if the revision is too broad, it may dilute the purpose of affordability.

In simple words, India may need a new definition of affordable housing because the old numbers may no longer reflect today’s reality. Home loan sizes have increased, property prices have moved up, and the cost of borrowing has changed the equation for buyers.

The larger message is this: affordable housing cannot remain frozen while the market changes around it. If policy wants to support real homebuyers, the definition must reflect real prices, real EMIs and real city-level conditions. For millions of families trying to buy their first home, this debate could become much more important than it appears at first glance.

Leave a Reply