Mumbai’s commercial real-estate market has always had a certain reputation. It has long been seen as the city of established business districts, landmark towers, financial institutions, and premium office addresses that symbolize corporate status as much as workplace function. But something important is now changing beneath that familiar image. The newer story is no longer only about legacy office zones. It is increasingly about micro-markets that are expanding the city’s commercial map and reshaping where growth is happening. That is why Mumbai’s office-market momentum matters right now. It is not just about higher leasing. It is about the city finding new pockets of commercial energy.

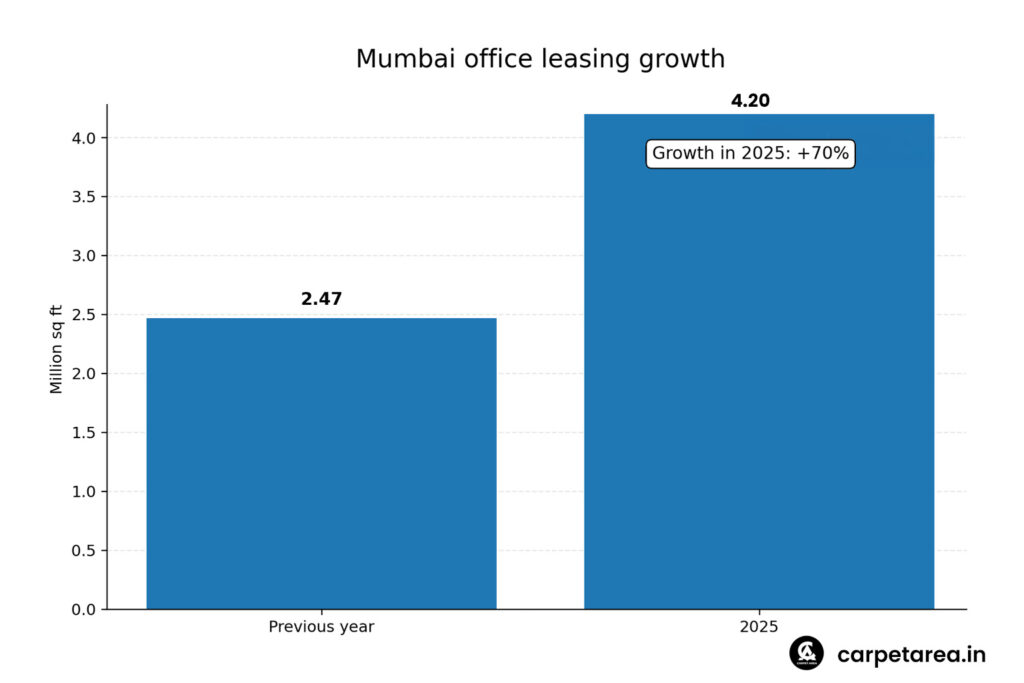

This shift becomes clearer when you look at the numbers. In 2025, India’s commercial real-estate market recorded 83.3 million sq ft of gross leasing activity, according to reporting that cited JLL data. Within that broader national growth story, Mumbai emerged as one of the standout markets, recording over 4.2 million sq ft of office leasing and registering roughly 70 percent growth from the previous year. That is not a small improvement. It is a strong indication that occupier interest in the city has deepened in a meaningful way. For a market often seen as expensive, space-constrained, and difficult to navigate, that kind of jump suggests that companies still see compelling value in being present in Mumbai.

But the real question is this: why is Mumbai seeing this push now? The answer appears to lie in structural change more than short-term excitement. The latest coverage suggests that growth is increasingly being driven by the rise of new commercial micro-markets that are attracting businesses from global finance, technology, and trade. That matters because office demand today is not driven only by the prestige of a pin code. Companies are thinking more carefully about access, quality, flexibility, infrastructure, employee convenience, and long-term expansion. When those preferences change, the commercial map of a city changes with them. Mumbai’s newer micro-markets seem to be benefiting from exactly this shift.

This is an important development because Mumbai has never lacked business demand. What it has often lacked is easy room to absorb that demand efficiently. Older business districts carry prestige, but they can also come with high costs, limited fresh stock, and more rigid locational constraints. Newer micro-markets, by contrast, can offer a different commercial proposition. They may provide modern Grade A stock, larger floor plates, better integrated infrastructure, and in some cases a more future-ready ecosystem for occupiers that want both brand value and operational efficiency. That is why the idea of micro-market growth is so important. It suggests that Mumbai is no longer relying only on old commercial strength. It is building new commercial nodes as well. This is an inference drawn from the reported shift in occupier preference toward premium and investment-friendly emerging zones.

Another reason this story stands out is that it fits into a larger pattern across India’s office market. Strong commercial leasing is increasingly being supported by deeper occupier diversity, expansion by global firms, and the need for better-quality workspaces. Mumbai’s role in that environment remains unique because it combines financial depth with broad economic relevance. Reporting cited in the same coverage notes that Mumbai contributes about 6.16 percent to India’s GDP, underlining why the city continues to anchor commercial activity at a national level. A city with that kind of economic weight does not stop mattering just because newer office hubs have emerged elsewhere. Instead, it adapts, and in this case that adaptation appears to be happening through the rise of new business micro-markets.

The interesting part is that this is not only a finance story. The new micro-market trend appears to be linked to demand from multiple sectors, especially finance, technology, and trade. That broadens the base of office demand and makes it more resilient. A market that depends too heavily on one sector can become vulnerable if that sector slows. But when several types of occupiers are active at the same time, the leasing story becomes stronger and more durable. That is one reason Mumbai’s recent commercial movement deserves attention. It is not being driven by a single wave of speculative interest. It appears to be supported by a wider corporate shift toward better-located, better-connected, and better-equipped office environments. This reading is based on the sector mix referenced in recent reporting.

Infrastructure also matters here, perhaps more than ever. One of the reasons micro-markets rise in importance is that a city’s infrastructure begins to change what feels accessible and practical. Mumbai is currently in the middle of a very large infrastructure push involving metro networks, expressways, airport-linked growth, and broader regional connectivity. ET has described this decade as one of Mumbai’s biggest infrastructure pushes yet, with more than $60 billion being invested in transport and connectivity systems. In commercial real estate, infrastructure is never just a background story. It shapes commuting patterns, improves business confidence, and changes which parts of the city can attract premium occupiers. That broader transformation helps explain why newer office micro-markets are becoming more commercially credible.

For developers and landlords, this trend brings both opportunity and pressure. The opportunity is obvious: when occupiers begin exploring newer locations, the commercial map opens up. That creates room for new office supply, better business parks, mixed-use formats, and longer-term land value creation. But the pressure is equally real. Occupiers today are more selective. They are not just looking for any office box in any corridor. They increasingly want Grade A quality, sustainability features, strong amenities, and buildings that support hybrid work realities. If Mumbai’s new micro-markets are to keep their momentum, they will need to deliver not just on location but on product quality as well. This is an inference, but it is consistent with the broader shift in occupier preferences noted in the recent coverage.

For investors, the story is especially interesting because it changes the city’s commercial growth equation. Traditionally, premium commercial confidence in Mumbai was heavily linked to a small cluster of established districts. Now, if micro-markets are beginning to lead the next phase of growth, the city’s investment story becomes wider. That creates room for capital to move into new office zones, redevelopment opportunities, and mixed-use commercial clusters that might not have drawn the same attention earlier. In practical terms, that can make the market more dynamic. It also means investors will need to read Mumbai more carefully, not as one office market, but as a set of evolving commercial pockets with different strengths and demand drivers. This is an inference based on the reported emergence of micro-markets as investment magnets.

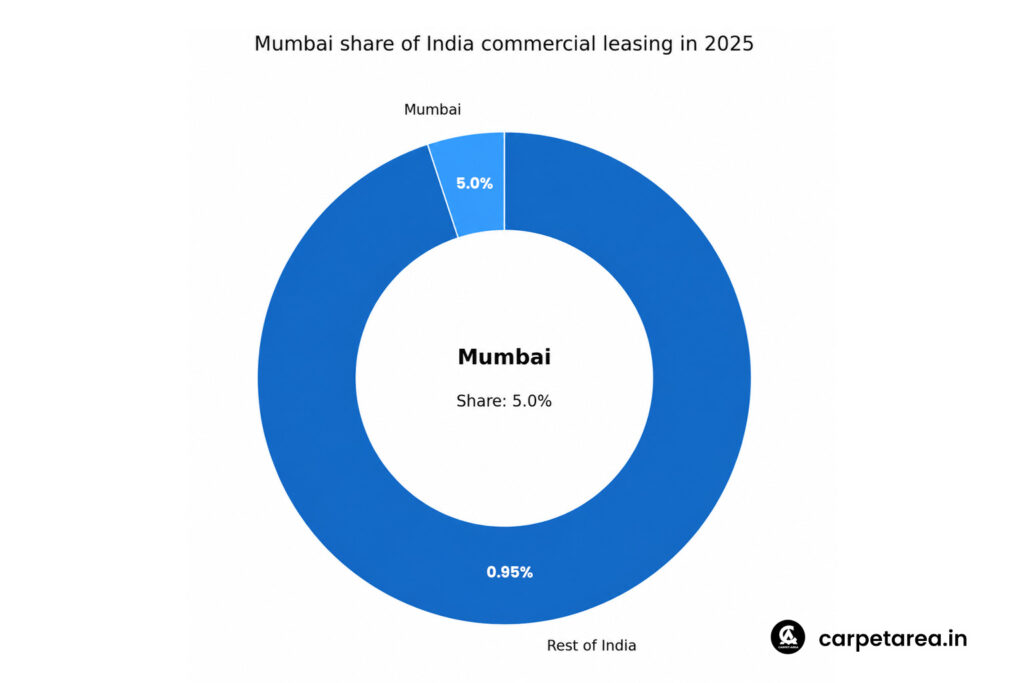

There is another important layer here. Mumbai’s commercial story is no longer only about holding its position as India’s financial capital. It is also about staying relevant in a much more competitive office-market environment. Bengaluru, Hyderabad, and NCR all have strong leasing stories of their own. So when Mumbai records over 4.2 million sq ft of leasing and about 70 percent annual growth, that is not just routine progress. It is evidence that the city is still able to compete for major office demand even as occupiers have more options across India. The emergence of stronger micro-markets may be exactly what is helping Mumbai stay in that race.

For ordinary readers, the biggest takeaway is simple. A city’s office market is not just about towers and rents. It often signals which parts of the city are becoming more important for jobs, investment, and daily business life. When commercial leasing strengthens in newer micro-markets, it usually means those areas are becoming more central to the city’s future. Over time, that can influence everything from residential demand and retail expansion to traffic flows and infrastructure priorities. So this is not a niche commercial-property update. It is also a city-growth story.

In the end, Mumbai’s new office micro-markets matter because they show how a mature city keeps reinventing itself. The city’s commercial identity is no longer being carried only by old business districts and legacy prestige. It is being renewed through emerging office zones that are drawing interest from finance, technology, and trade, backed by infrastructure change and evolving occupier priorities. That is why this story deserves attention. Mumbai’s office market is not just growing. It is spreading, adapting, and becoming more layered. And in commercial real estate, that is often a sign of a city entering its next serious phase of growth.

Leave a Reply