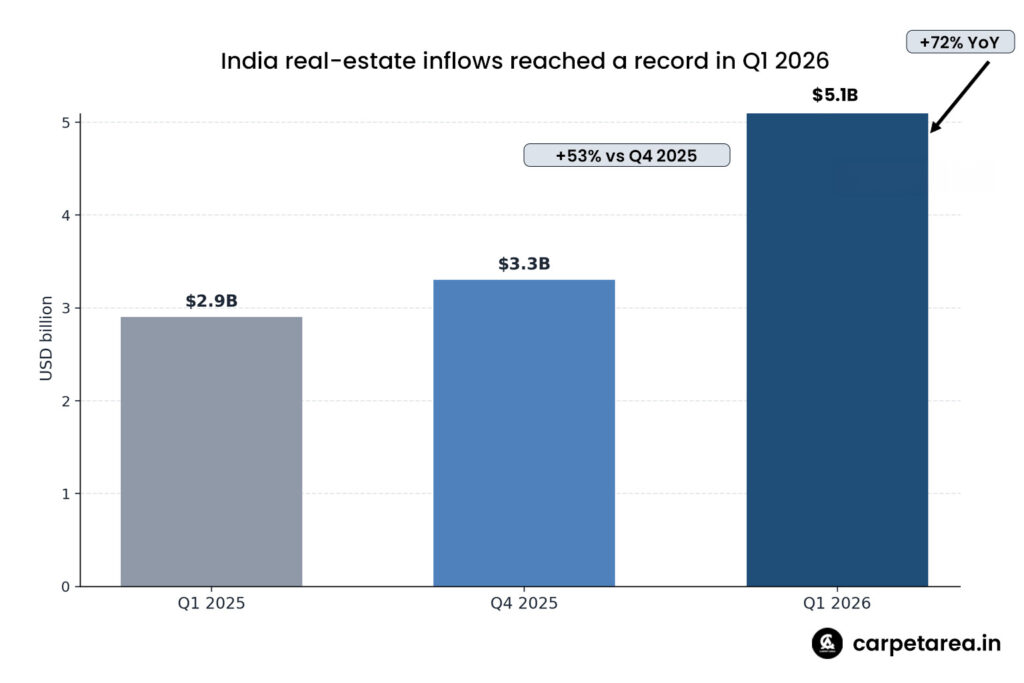

India’s real-estate sector has started 2026 with a number that is big enough to attract attention on its own, but the real story lies in what sits behind it. Capital inflows into Indian real estate rose to a record $5.1 billion in Q1 2026, up 72 percent year on year from $2.9 billion in the same quarter last year. On a sequential basis too, the market moved sharply higher, with inflows rising 53 percent from $3.3 billion in Q4 2025. That makes this not just a strong quarter, but the highest quarterly investment recorded in the sector so far.

At first glance, a record investment number may sound like a story meant only for investors, developers, or financial analysts. But it matters to a much wider audience than that. Real-estate capital does not stay limited to boardrooms. It affects what gets built, which projects move faster, which cities attract more attention, and what kind of supply reaches the market. When a sector attracts money at this scale, it usually means confidence is not just surviving, but deepening. That is why this Q1 number matters. It is a signal that despite global uncertainty, India’s real-estate market is still being seen as a place where serious capital wants to participate.

What makes the story more interesting is that this is not a vague flood of money chasing anything and everything. The inflows were concentrated in areas that tell us a lot about where investors currently see value. According to CBRE’s market monitor and coverage based on it, a large part of the quarter’s money went into built-up office assets and land or development-site acquisitions, and together these accounted for more than 90 percent of total equity inflows. In simple terms, investors were not just placing broad bets on real estate as a theme. They were focusing on assets that either generate income now or create a pipeline for future development.

That distinction matters because it shows this is not just an emotion-driven rally. Office assets are generally linked to rental income, occupancy strength, and institutional-grade quality. Land and development sites, on the other hand, represent confidence in the next phase of the market, especially in residential and mixed-use segments. In fact, Business Standard reported that over 73 percent of land-acquisition capital during the quarter was deployed for mixed-use and residential projects, with the rest going into office, warehousing, and hospitality developments. That gives this story an important second layer: investors are not only backing current income. They are also backing future city growth.

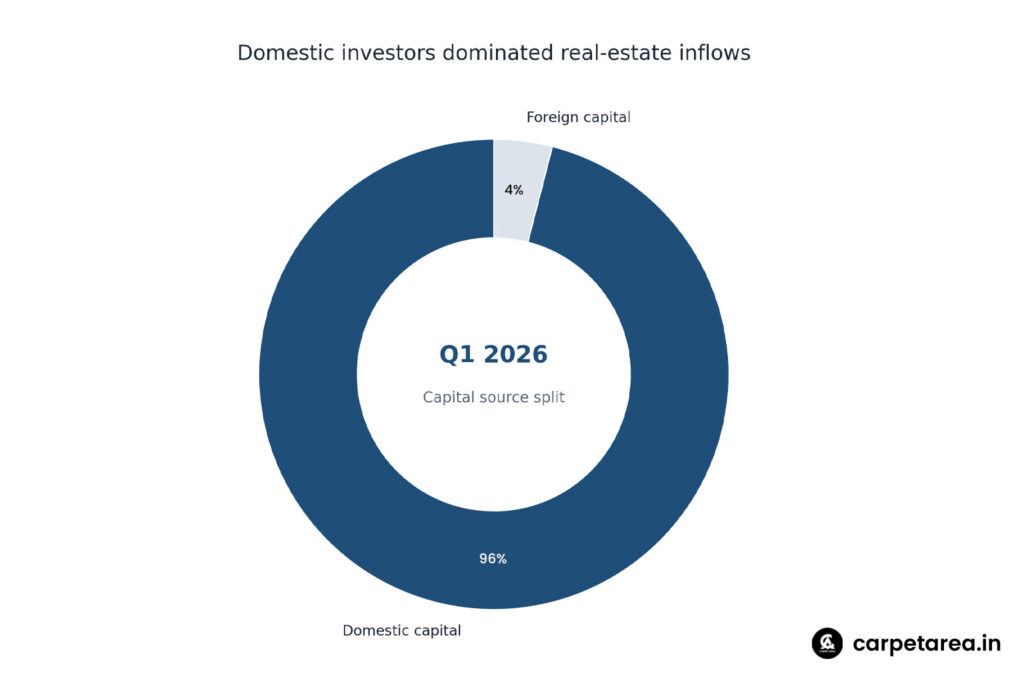

Another reason this quarter stands out is the nature of the money behind it. The biggest driver was not foreign capital chasing India as a trendy emerging market trade. It was domestic capital. Reports based on the CBRE data show that domestic investors accounted for about 96 percent of total inflows in Q1 2026. That is an unusually strong local vote of confidence. It suggests that Indian capital is becoming more willing to support Indian real estate at scale, even at a time when global macro conditions remain unsettled. For the sector, that is important because domestic money is often seen as more patient, more market-aware, and more closely tied to local fundamentals.

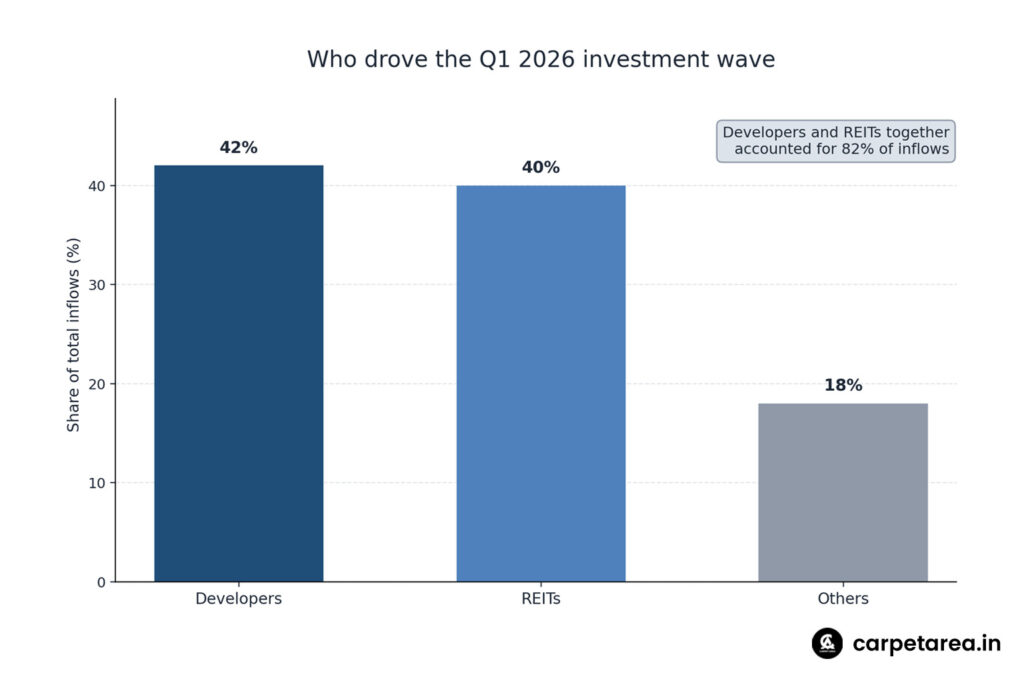

The composition of investors tells its own story as well. Developers accounted for 42 percent of total inflows, while REITs contributed around 40 percent, meaning those two groups together made up over 80 percent of all investments during the quarter. REIT investment alone crossed $2 billion, which is a sharp rise and a strong sign of institutional appetite for income-generating assets. This is significant because it shows two different forms of confidence operating at the same time. Developers are willing to deploy capital into future growth, while REIT-linked activity points to continued comfort with stabilized, yield-oriented real estate. That combination makes the quarter look broader and healthier than a one-dimensional investment spike.

For buyers and ordinary readers, this may raise a fair question: if so much money is entering the sector, does that automatically mean better outcomes for the market? Not always. More investment does not instantly make homes more affordable or ensure every project will succeed. But it does increase the chances that stronger projects will move forward with greater confidence and better funding support. It can also improve market depth by creating new platforms, unlocking land, and supporting the development of better-quality assets. ET Realty reported that the quarter also saw the creation of new investment and development platforms worth about $234 million, especially around residential-led opportunities. That suggests the money is not just being parked. It is being organized for future deployment.

The city pattern behind the investment wave also matters. Bengaluru, Mumbai, and Delhi-NCR together accounted for around 65 percent of the total inflows. That tells us the market is still rewarding scale, maturity, and established urban demand. Investors may be exploring more geographies than before, but when it comes to very large commitments, the biggest cities still dominate. This is not surprising. These markets offer depth, absorption, office demand, and development visibility that smaller cities often cannot yet match. Still, the concentration of capital also means that the next phase of India’s real-estate growth will continue to be shaped heavily by these major urban centres.

There is also a larger market signal buried inside this record. India’s real estate is increasingly looking less like a cyclical story driven only by housing sentiment and more like a multi-layered investment class. Office assets, REIT activity, land buying, mixed-use development, residential platforms, and institutional structures are all now part of the same conversation. That shift matters because mature real-estate markets usually attract serious long-term capital only when investors can participate across different formats and risk levels. Q1 2026 appears to show exactly that kind of evolution. This is partly an inference, but it is supported by the diversity of capital deployment seen in the reported data.

At the same time, it is worth keeping some perspective. A record quarter does not mean every part of the market is equally strong. Investment inflows can be concentrated in select asset classes and top cities while affordability pressures continue elsewhere. Residential buyers in several markets are still dealing with higher prices and more cautious conditions. Office demand remains strong, but it is strongest in specific cities and sectors. So this is not a story that says every corner of Indian real estate is booming equally. It is better understood as a story of selective confidence. Capital is flowing strongly, but it is flowing toward what investors see as the safest and most promising parts of the market.

That is exactly why the domestic-capital angle matters so much. When local investors dominate a quarter like this, it often reflects judgment built on proximity, not distance. Domestic institutions and market participants tend to know where the real demand is, where the stronger developers are, and which asset classes are likely to hold up. Their willingness to commit so heavily suggests that the market’s core fundamentals are being viewed as durable rather than temporary. It also makes India’s real-estate story look less dependent on foreign sentiment swings, which is a meaningful shift in itself.

For developers, the message is encouraging but demanding. Capital is available, but it is clearly moving toward quality, structure, and credible opportunity. Projects that are well located, properly planned, and aligned with real demand are likely to find support more easily than weaker or speculative plays. For investors, the message is that Indian real estate is no longer just a broad emerging-market narrative. It is a sector where income assets and development opportunities can coexist in the same growth story. For buyers, the takeaway is more indirect but still important: when the sector attracts capital at this level, it usually means more organized development, stronger funding pipelines, and a better chance that serious projects will keep moving.

In the end, the most important thing about the $5.1 billion figure is not the size of the headline alone. It is what the quarter reveals about India’s real-estate market. It reveals that domestic confidence is strong, that institutional participation is deepening, that office and development assets remain attractive, and that the market is being treated less like a short-term trade and more like a serious long-term opportunity. That is why this Q1 record matters. It is not just a number to celebrate. It is a sign that real estate in India is entering a more mature, better-capitalized, and more strategically backed phase of growth.

Leave a Reply