Hyderabad’s property market is used to talking about demand, new launches, infrastructure growth and premium corridors. But this time, one of the biggest conversations in the city is not about a flashy project or a hot micro-market. It is about a policy rule that many ordinary buyers may never even have heard of before: TDR. On paper, Telangana’s revised Transferable Development Rights framework looks like an urban-planning tool. In the market, though, it is now being discussed as a rising-cost problem. Builders say the new system is pushing up TDR prices sharply and making projects, especially high-rises, more expensive to plan.

To understand why this story matters, it helps to start with the basics. TDR is a development-right certificate given to landowners when their land is taken for public works like road widening, flyovers, nala works, or other infrastructure projects. Instead of only paying direct cash compensation, the government can compensate landowners by giving them development rights that can later be used or sold. In theory, that is a practical model. The government reduces the direct cash burden of land acquisition, while landowners get a tradable benefit. That is the original logic behind TDR.

The real tension began when TDR moved from being an optional planning tool to becoming more deeply tied to the economics of construction. Telangana’s amended building rules expanded the use of TDR and, for certain kinds of construction, made it effectively unavoidable. Under the revised rules, buildings between 10 and 20 floors must load 3 percent TDR on the area above the 10th floor, while buildings above 20 floors must load 5 percent beyond the 20th floor. The rules also allow TDR in certain setback relaxations, and developers must submit 50 percent of the required TDR at the building-permission stage and the remaining 50 percent before the occupancy certificate.

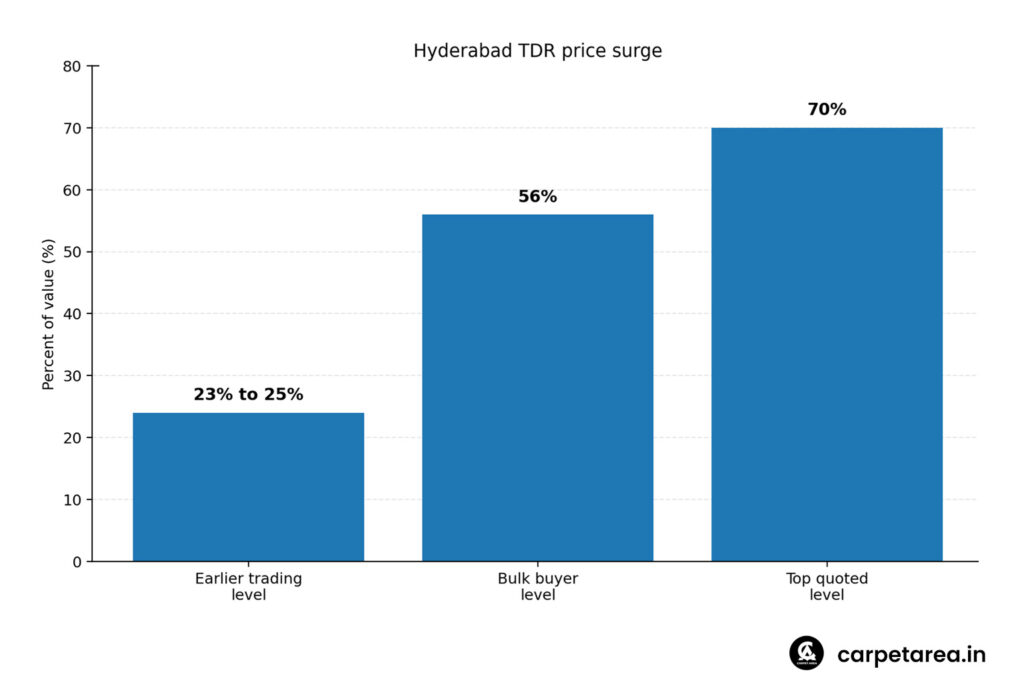

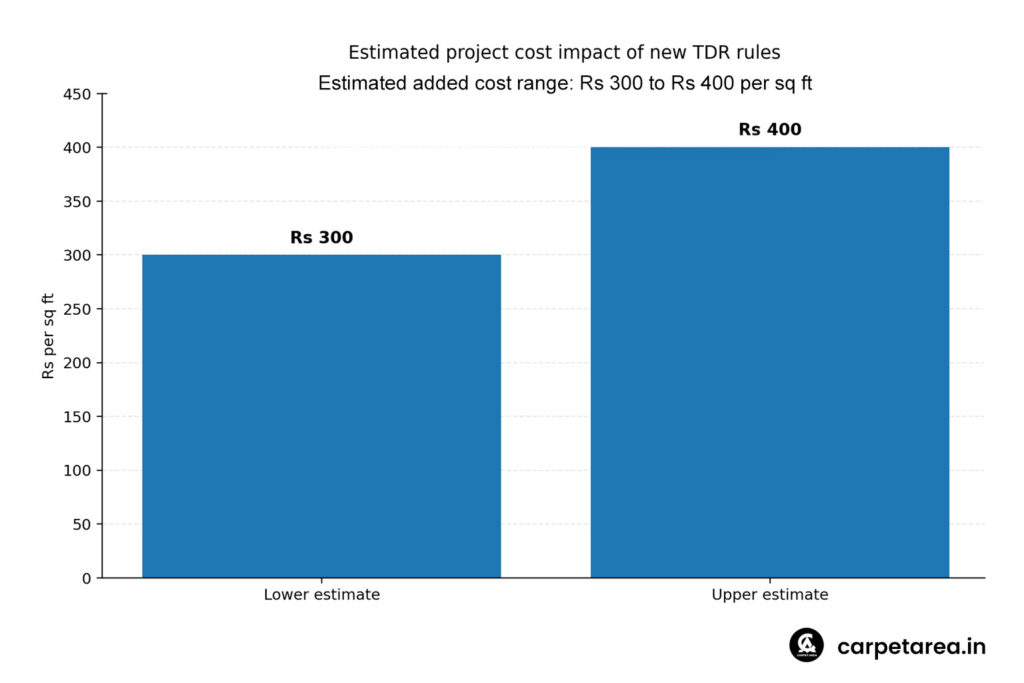

That is where a technical rule turned into a market issue. Once demand for TDR became structurally linked to permissions and project design, prices started rising fast. The Times of India reported that TDRs that were earlier trading at roughly 23 percent to 25 percent of value were now being quoted as high as 70 percent in some cases, while bulk buyers were getting them at around 56 percent. That is a very sharp move for something that now directly affects how certain projects can be built. Earlier coverage also said builders estimated that the new TDR regime could add roughly Rs 300 to Rs 400 per sq ft to construction costs in some cases. In a city where project economics already depend on careful cost control, that is not a small shift.

This is why the builder reaction has been so strong. Their complaint is not only that TDR has become more important. Their bigger concern is that a policy-driven input is now rising rapidly in price. When a project needs more TDR, and the market price of that TDR shoots up, the developer has very little room to escape the cost. Something has to give. Either margins shrink, launch prices change, project planning becomes more conservative, or certain development formats become less attractive. In other words, the policy may not have been designed to raise project costs, but in practice that is exactly how many builders are now experiencing it. This is an inference based on the reported TDR price surge and the estimated cost impact cited in market coverage.

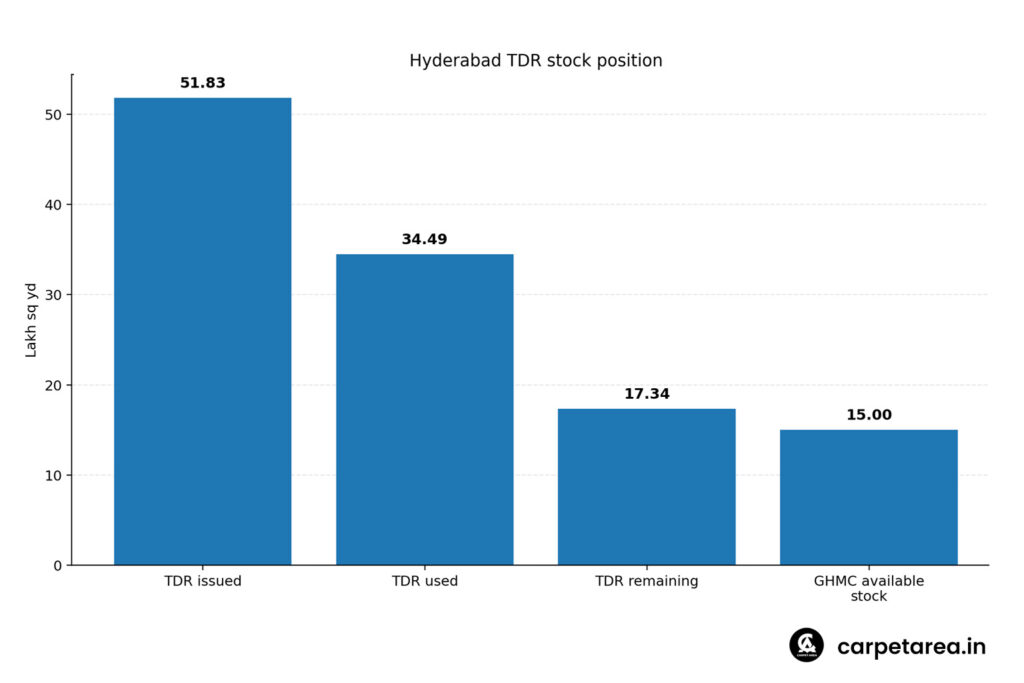

What makes the situation even more interesting is that the issue does not appear to be a simple lack of available TDR on paper. The Times of India reported that GHMC had more than 15 lakh square yards of TDR available, equivalent to roughly 316 acres, and that builders themselves said this could be enough to meet Greater Hyderabad’s built-up demand for the next two to three years. The same report said that since 2017, TDRs covering 51.83 lakh square yards had been issued to 1,585 property owners, with 34.49 lakh square yards already used. Later reporting said 1,967 individuals had received TDRs and that nearly Rs 9,000 crore worth of TDR was available in the market. So the immediate mystery is obvious: if such a large volume exists, why are prices rising so sharply?

That question has led to a more uncomfortable part of the debate. According to The Times of India, some residents and market participants alleged that large quantities of TDR may have accumulated with a relatively small group of players, creating a scarcity effect even though substantial stock officially exists. The paper cited allegations about hoarding, benami holding, and cartel-like behaviour. These are allegations reported in the press, not adjudicated findings, and that distinction matters. But even as allegations, they help explain why the issue has become more than just a policy argument. Once the market begins to suspect that prices are rising not only because of rules but also because of concentration and control, the discussion shifts from cost to credibility.

At the same time, the government’s side of the story cannot simply be dismissed. From the state’s perspective, encouraging greater TDR use is not just about helping builders build more. It is also about compensating landowners without putting the entire burden on public finances. Earlier reporting noted that if landowners rejected TDR and demanded cash compensation instead, the state could face around Rs 5,000 crore in cash outgo over two years. In that context, promoting TDR is also a fiscal strategy. Later amendments under GO 95 were welcomed by CREDAI Hyderabad as well, which said the changes provided more clarity and reduced upfront capital burden by allowing staggered TDR submission. So this is not a clean story of one side being entirely right and the other entirely wrong. It is a clash between policy intent and market consequences.

That is exactly what makes this such a strong real-estate story. It is not just about whether TDR is good or bad. It is about whether a rule designed to improve land compensation and urban development is now creating side effects that the market was not ready for. On paper, giving landowners tradable development rights sounds efficient. In practice, when those rights become costly and essential, they stop feeling like a planning tool and start feeling like a project input that can distort pricing. Hyderabad is now in that awkward zone where the logic of the policy may still make sense, but the market impact is becoming harder to ignore.

For ordinary buyers, this may sound distant at first. Most buyers will never read a government order on TDR loading, and almost none will calculate how a 3 percent or 5 percent TDR requirement affects a tower design. But buyers do feel the outcome when costs rise, launches get repriced, or supply decisions change. That is why even a technical rule can eventually become a consumer issue. If project economics tighten too much, someone in the chain usually carries that burden. Sometimes it is the builder through lower margins. Sometimes it is the landowner through changed deal structures. And in many cases, over time, some of it reaches the buyer through higher prices or more cautious project offerings. That is an inference, but it is a realistic one in a market where a compulsory development input is becoming more expensive.

For developers, the bigger lesson is about how quickly policy can change the math of real estate. Hyderabad remains one of India’s most closely watched city markets, and it still has demand, ambition, and growth potential. But this episode is a reminder that project viability is shaped not only by land cost and buyer demand, but also by the design of policy itself. When approvals, setbacks, height limits, and development rights are reworked, the economics of the city shifts too. Some projects may still move smoothly, especially for better-capitalised players. Others may need to rethink height, phasing, or location strategy. That is how a rulebook change slowly becomes a supply-side story.

In the end, Hyderabad’s TDR story matters because it shows how urban policy can reshape real-estate economics almost overnight. A tool meant to compensate landowners and support infrastructure-led development is now being viewed by many builders as a cost escalator. The city may still adjust, the market may still absorb the change, and the policy may still achieve some of its intended goals. But right now, the signal from the market is clear: this transition is not painless. Builders are worried about cost, the public is hearing allegations of scarcity despite official stock, and buyers may eventually feel some of the consequences indirectly. That is why this is not just a niche policy story. It is one of the clearest recent examples of how rules on paper can quickly become price pressures on the ground.

Leave a Reply