The NCR property market is entering a phase that looks confusing on the surface but makes complete sense once you look closer. Prices are still moving up in several key corridors, yet the pace of buying is no longer as aggressive as it was during the post-pandemic boom. That combination matters because it tells us the market is not collapsing, but it is definitely changing. For buyers, developers, and investors, the bigger story is no longer just growth. It is about how sustainable that growth really is.

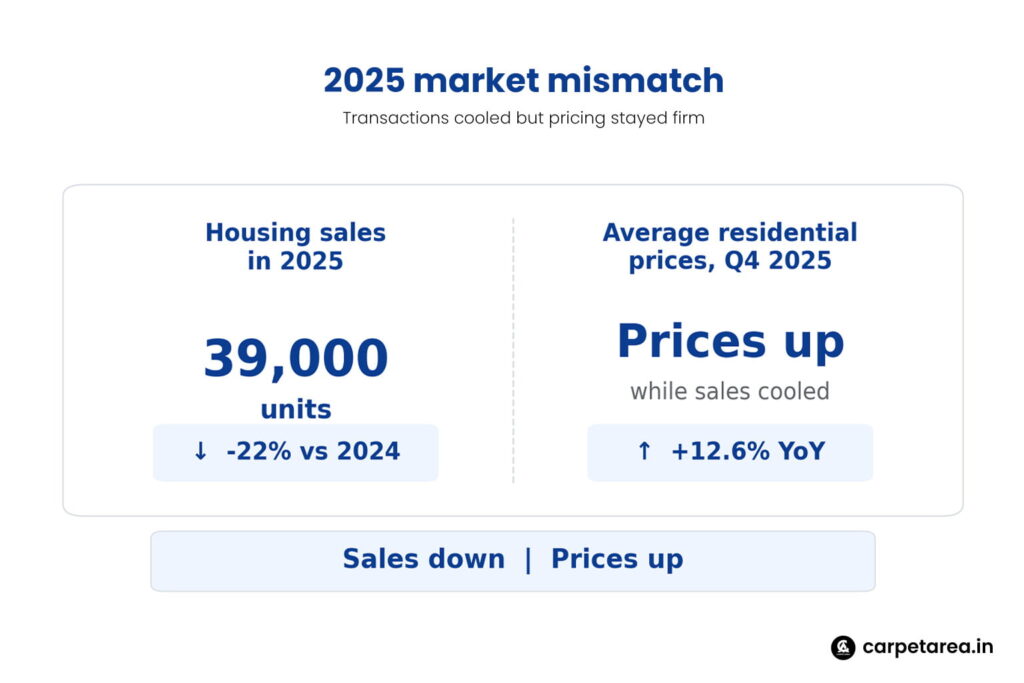

Recent reporting shows that Delhi-NCR has started showing signs of moderation even though pricing remains firm. JLL data cited by Realty+ said NCR’s housing sales in 2025 were around 39,000 units, down almost 22 percent from 2024, while average residential prices in the fourth quarter were still up 12.6 percent year on year. In simple terms, transactions cooled, but values did not fall with them. That is the kind of mismatch that usually grabs attention because it suggests demand is becoming more selective rather than disappearing altogether.

The first thing buyers need to understand is that a sales slowdown does not always lead to an immediate price correction. In NCR, especially in high-visibility corridors, pricing is being supported by a very different mix of supply and demand than what the market saw a few years ago. Some of the strongest activity continues to come from micro-markets such as Dwarka Expressway, Sohna Road, Yamuna Expressway, New Gurugram, and Raj Nagar Extension. These locations are still benefiting from infrastructure-led optimism, better connectivity, and a perception of long-term value. So even if overall demand has cooled, well-positioned pockets are still able to hold prices up.

There is also a second layer to this story. A lot of fresh supply in Delhi-NCR has moved toward higher-ticket projects, especially in Gurugram and Noida. PropEquity data reported by Financial Express showed that in Q1 2026, Delhi-NCR recorded 12,141 housing sales, up 13 percent year on year, but down 1 percent quarter on quarter, while supply jumped 89 percent year on year to 17,227 units. The same report noted that Delhi-NCR saw more supply than several traditionally high-supply cities, but absorption remained weaker than Bengaluru because high-ticket launches affected sales. That matters because it means the market is active, but not every new launch is being absorbed with equal ease.

This is where the current phase becomes especially important for homebuyers. When prices rise quickly for several years and fresh launches move increasingly upward in value, the market starts filtering out casual buyers. Only those with stronger budgets, higher conviction, or a long-term purchase plan remain active. Everyone else becomes more cautious. That is one reason the NCR market now feels more selective. It is not that buyers have vanished. It is that the pool of buyers willing or able to transact at current price points has become narrower. That interpretation is consistent with the rise in premium supply, softer absorption, and growing caution described in recent market coverage.

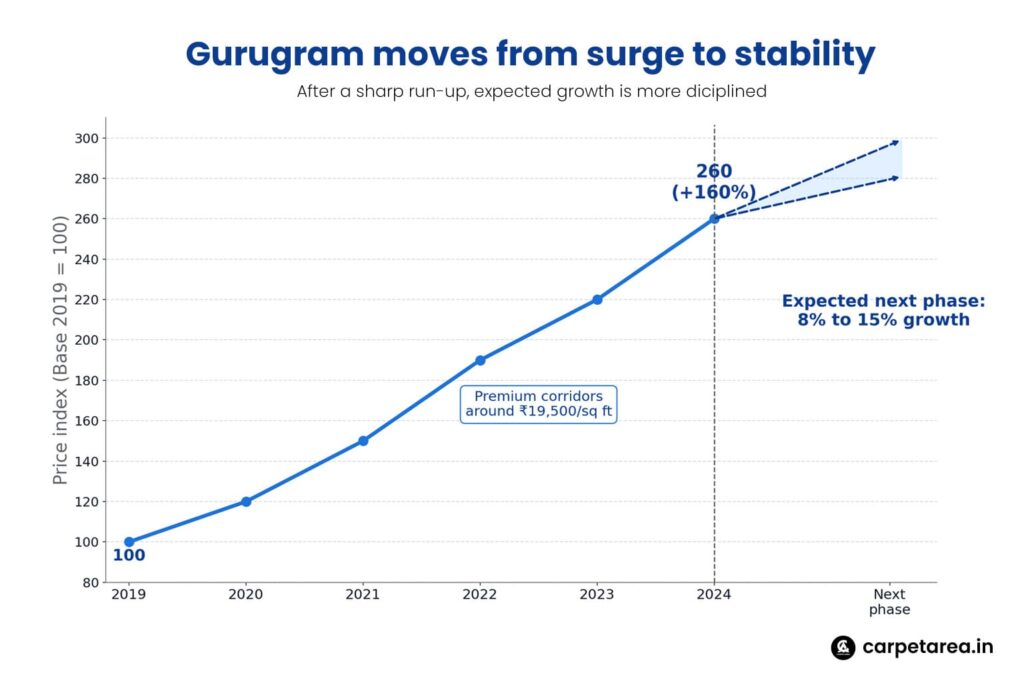

Gurugram is a good example of this shift. The Tribune, citing CBRE’s India Residential Market Outlook, reported that key Gurugram micro-markets saw property prices rise nearly 160 percent between 2019 and 2024, reaching around ₹19,500 per sq ft in premium corridors. At the same time, the report suggested that the market is now moving into a more stable phase, where income growth is starting to catch up and affordability pressures may ease slightly. Prices are still expected to rise in high-demand zones, but more in the range of 8 to 15 percent, not in the kind of speculative spikes seen earlier. That suggests the era of sharp runaway appreciation may be giving way to a more disciplined market.

For developers, this creates a very different operating environment. During a hot cycle, pricing momentum itself can carry demand for a while. In a more mature cycle, developers have to work harder. Product quality, location, project credibility, payment structure, and brand trust become more important than headline appreciation alone. Economic Times reported that some NCR developers have started delaying launches, offering incentives, or even exiting commitments as weak demand and rising cash flow pressure begin to show. That is a sign that the market is no longer rewarding every project equally. Better-capitalised and established developers may still perform well, but weaker players are more exposed when demand becomes cautious.

For buyers, this is not necessarily bad news. In fact, a selective market can sometimes be a healthier one. When the frenzy cools, purchase decisions become more rational. Buyers compare pricing more carefully, evaluate possession risk more seriously, and think more clearly about whether they are buying for use or for appreciation. That often leads to better market discipline. It also forces projects to compete on real value rather than only on market buzz. If you are an end user, this phase can actually offer a better decision window than a highly overheated one. That is an inference based on the reported moderation in sales, stabilising affordability trends, and growing buyer selectivity.

The larger takeaway is that NCR is not really in a simple slowdown story. It is in a sorting phase. Strong micro-markets are holding up. Prices are still rising in important corridors. But the market is no longer lifting all boats at the same speed. Sales are softer in aggregate, supply is becoming more uneven, and high-ticket launches are exposing the gap between what is being built and what the broader buyer base can comfortably absorb. That is why this phase feels mixed. The market still has strength, but it is no longer effortless strength.

In the end, the NCR housing story right now is less about contradiction and more about transition. Prices rising despite slower sales does not mean the market is irrational. It means the market is adjusting after a period of rapid appreciation. For homebuyers, that means caution is justified, but so is opportunity in the right micro-market. For developers, it means momentum alone is no longer enough. And for the wider real-estate sector, it is a reminder that when a market matures, the most important shift is not always in price. Sometimes it is in buyer behaviour.

Leave a Reply