A conventional homebuyer usually studies the location, carpet area, construction quality and price per square foot.

A senior living investor must look beyond the apartment.

The person who eventually occupies that home may not judge it only by the flooring, balcony or clubhouse. Daily food quality, staff behaviour, emergency response, healthcare support and community life may matter much more.

This is what makes senior living investment in India different from ordinary residential real estate.

The investor may purchase a physical property, but its long-term demand will depend heavily on the services and operating system built around it.

Why senior living is attracting investor attention?

India’s population is ageing.

According to the India Ageing Report 2023, the country had approximately 149 million people aged 60 and above in 2022. This population is projected to reach around 347 million by 2050, representing approximately 20.8% of India’s population.

At the same time:

- children are moving to different cities and countries;

- nuclear families are becoming more common;

- urban seniors are living longer;

- healthcare and daily-support requirements are increasing;

- and financially independent retirees are becoming more willing to pay for convenience and community.

This does not mean every senior citizen will move into an organised senior living community. India’s older population represents different income groups, health conditions and family arrangements.

However, even a small section of this population can create considerable demand because organised senior living supply remains limited.

JLL and the Association of Senior Living India have projected that the organised senior living market could reach approximately ₹64,500 crore by 2030. Their research also indicates significant growth potential because organised-market penetration remains low.

Senior living is more than a property product

A conventional apartment primarily offers:

- residential space;

- location advantages;

- building amenities;

- security;

- and potential capital appreciation.

A professionally managed senior living community may additionally offer:

- senior-friendly design;

- housekeeping;

- dining;

- organised activities;

- transportation;

- nursing assistance;

- emergency response;

- physiotherapy;

- medication support;

- and assisted-care services.

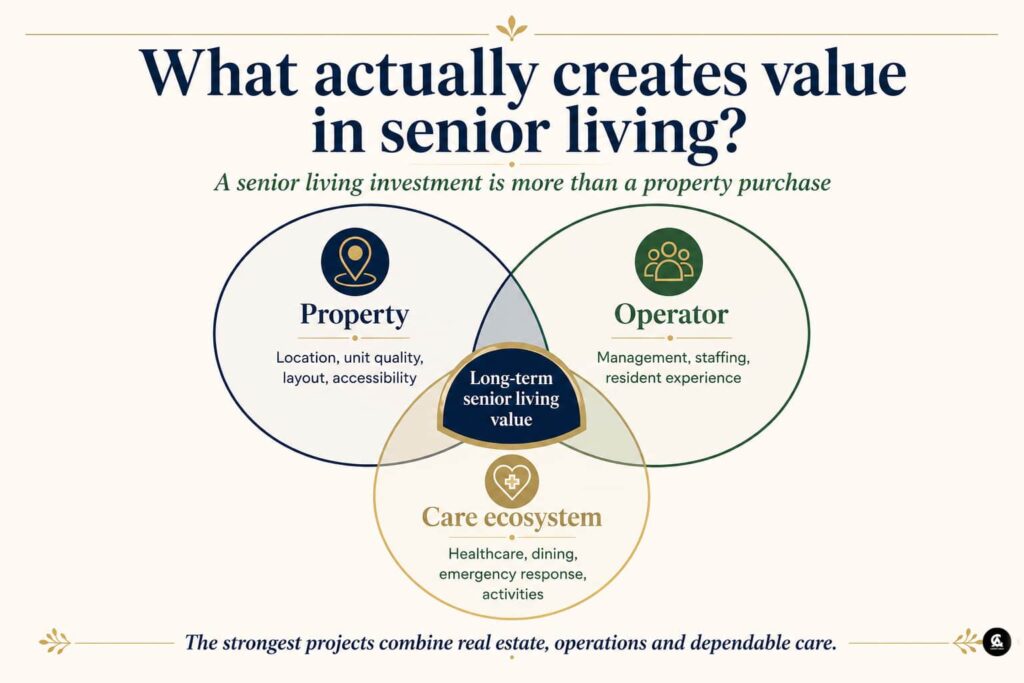

Senior living therefore brings together four different sectors:

Real estate, hospitality, healthcare and community management.

For an investor, this creates an important distinction.

The apartment and the operator cannot be evaluated separately.

A project may have excellent construction and a strong location. But if the food is poor, staffing is inconsistent, emergencies are mishandled or residents do not feel respected, occupancy and rental demand may decline.

Senior living versus a conventional apartment

Senior living should not be analysed with the same checklist used for a normal residential property.

| Factor | Conventional apartment | Senior living property |

|---|---|---|

| Buyer pool | Broad residential market | Seniors and their families |

| Rental demand | Primarily location-driven | Location and service-driven |

| Operator dependency | Usually limited | Often significant |

| Monthly expenses | Standard maintenance | Maintenance plus service charges |

| Resale market | Comparatively wider | More specialised |

| Healthcare relevance | Usually limited | A major differentiator |

| Property management | Building-focused | Building and care ecosystem |

| Resident experience | Mostly self-managed | Heavily influenced by the operator |

A narrower customer base does not automatically make senior living a weak investment.

It means that the project must solve a very specific problem for seniors and their families.

Where can investor returns come from?

Returns from a senior living investment can come from different sources.

Property appreciation

The underlying property may appreciate when the location develops, infrastructure improves and demand for senior housing grows.

However, appreciation should not be assumed merely because a project has been marketed as senior living.

Rental income

A unit may earn rental income from seniors who prefer managed accommodation without purchasing a home.

Rental performance will depend on:

- project occupancy;

- monthly service charges;

- operator quality;

- care availability;

- and the affordability of the complete package.

Longer occupancy periods

Older residents may prefer stable, long-term accommodation because frequent relocation becomes difficult with age.

This can reduce tenant turnover, but only when residents are satisfied with the services and community.

Managed-service premium

Residents may be willing to pay more for furnished accommodation that includes meals, housekeeping, safety and healthcare support.

Investors must verify whether this premium is received by the property owner, retained by the operator or divided between both.

Institutional growth

Developers, operators and investment platforms may benefit from the wider expansion of the senior care sector.

However, investing in an operating company is very different from purchasing an individual apartment.

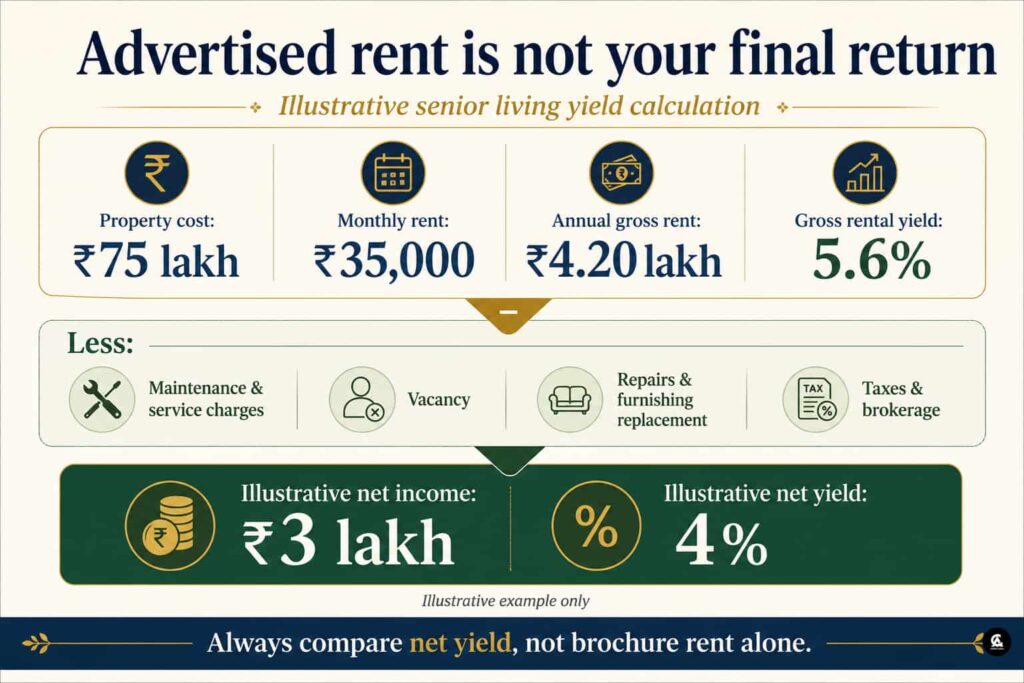

Advertised rent is not the final return

Consider a simple example.

Suppose an investor purchases a senior living apartment for ₹75 lakh and receives a monthly rent of ₹35,000.

| Calculation | Amount |

|---|---|

| Monthly rent | ₹35,000 |

| Annual gross rent | ₹4.20 lakh |

| Property cost | ₹75 lakh |

| Gross rental yield | Approximately 5.6% |

At first glance, a 5.6% rental yield may appear attractive.

But this is the gross yield.

The investor may still need to deduct:

- maintenance charges;

- service or operator fees;

- vacancy losses;

- furnishing replacement;

- repairs;

- brokerage;

- property tax;

- insurance;

- and applicable income tax.

If these expenses reduce the investor’s annual income to approximately ₹3 lakh, the illustrative net rental yield falls to around 4%.

The correct question is therefore not:

What rent is shown in the brochure?

The more useful question is:

What amount will reach the investor after all recurring expenses?

The biggest investment risk may be the operator

In ordinary housing, the owner or tenant can independently change domestic workers, cooks or service providers.

That may not be possible in an organised senior living community.

One operator may control:

- dining;

- housekeeping;

- nursing;

- emergency response;

- resident activities;

- transport;

- staffing;

- family communication;

- and grievance management.

This makes the operator central to the investment.

A poorly performing operator can weaken resident trust even when the building remains in excellent condition.

That can lead to:

Poor operations → dissatisfied residents → lower occupancy → weaker rental demand → pressure on resale value.

Before investing, ask:

- How many senior living projects does the operator manage?

- How long has it been operating?

- What is the current occupancy?

- How many residents renew their stay?

- How are emergencies handled?

- Who supervises the nursing and care teams?

- Can the developer replace the operator?

- What happens if the operator exits the project?

- Are service standards written into the agreement?

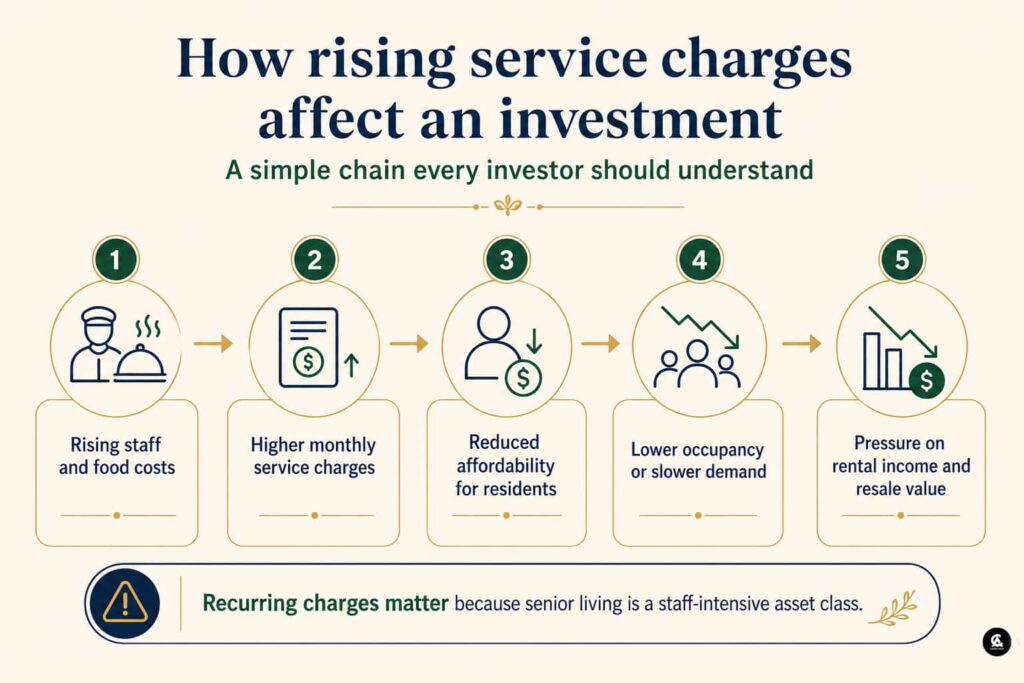

Rising service charges can weaken demand

Senior living is a staff-intensive business.

Its recurring expenses may include:

- salaries;

- food;

- electricity;

- nursing;

- transportation;

- maintenance;

- healthcare coordination;

- security;

- and resident activities.

These costs may rise over time.

If the operator increases monthly service charges rapidly, the overall package may become unaffordable for residents.

That can create a chain reaction:

Rising operating costs → higher service charges → lower affordability → reduced demand → pressure on rental income and resale.

Investors should request:

- the existing monthly service charge;

- services included in the fee;

- services charged separately;

- past increases;

- the future escalation formula;

- higher-dependency care charges;

- and penalties for delayed payment.

A low introductory price is not meaningful when future increases are not clearly controlled.

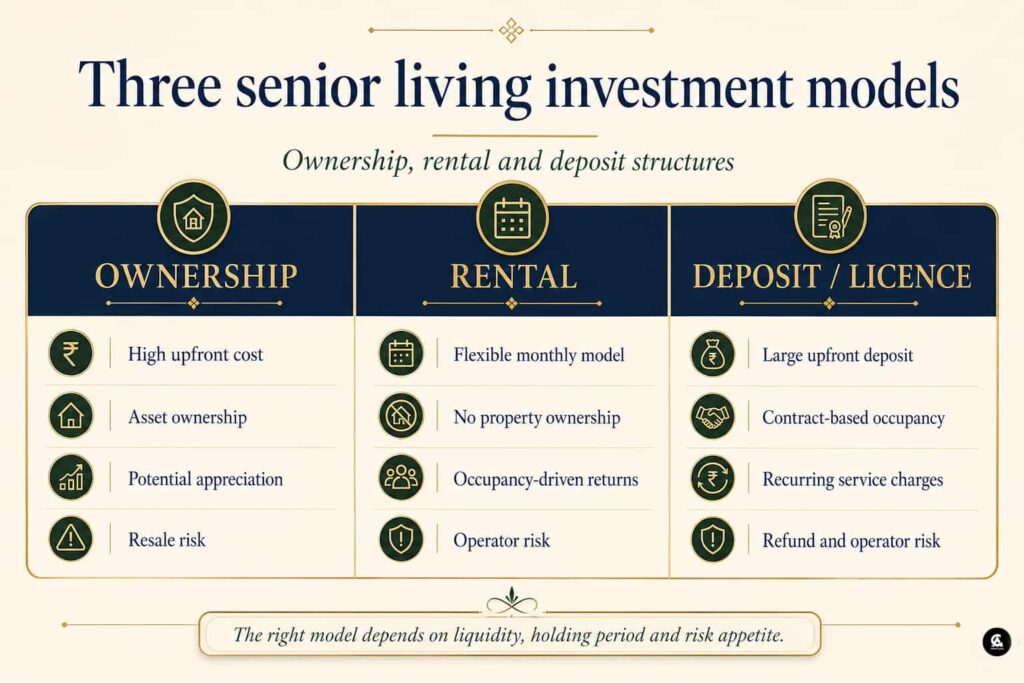

Ownership, rental and deposit-based models

Senior living projects in India may follow different commercial structures.

Understanding the legal and financial model is essential before investing.

Ownership model

The resident or investor purchases the property and continues paying maintenance and service charges.

Potential advantages include:

- property ownership;

- long-term residence;

- possible appreciation;

- and potential rental income.

Possible risks include:

- high upfront investment;

- specialised resale demand;

- mandatory service charges;

- and operator dependency.

Rental model

The resident pays monthly rent and service charges without purchasing the property.

This may offer:

- lower initial commitment;

- greater flexibility;

- trial-stay options;

- and easier relocation when care requirements change.

For investors and operators, however, the rental model depends on stable occupancy.

Deposit or licence model

Some projects may collect a substantial deposit with recurring monthly service charges.

Families and investors should examine:

- whether the deposit is refundable;

- the refund timeline;

- permitted deductions;

- the operator’s financial condition;

- and the legal nature of occupancy.

Resale and exit conditions need close examination

A senior living property may not have the same resale market as a conventional apartment.

Possible restrictions can include:

- minimum resident age;

- compulsory operator agreements;

- restrictions on independent leasing;

- mandatory service charges;

- transfer fees;

- operator approval for tenants;

- or limitations on self-use.

Before investing, check:

- Can the unit be sold to any buyer?

- Must the occupant meet a minimum age?

- Can the property be rented independently?

- Does the operator approve tenants?

- Is there a transfer fee?

- Does the developer have a first right to repurchase?

- Are there completed resale transactions within the project?

- How long did earlier resales take?

A projected appreciation figure has limited value when the exit mechanism is unclear.

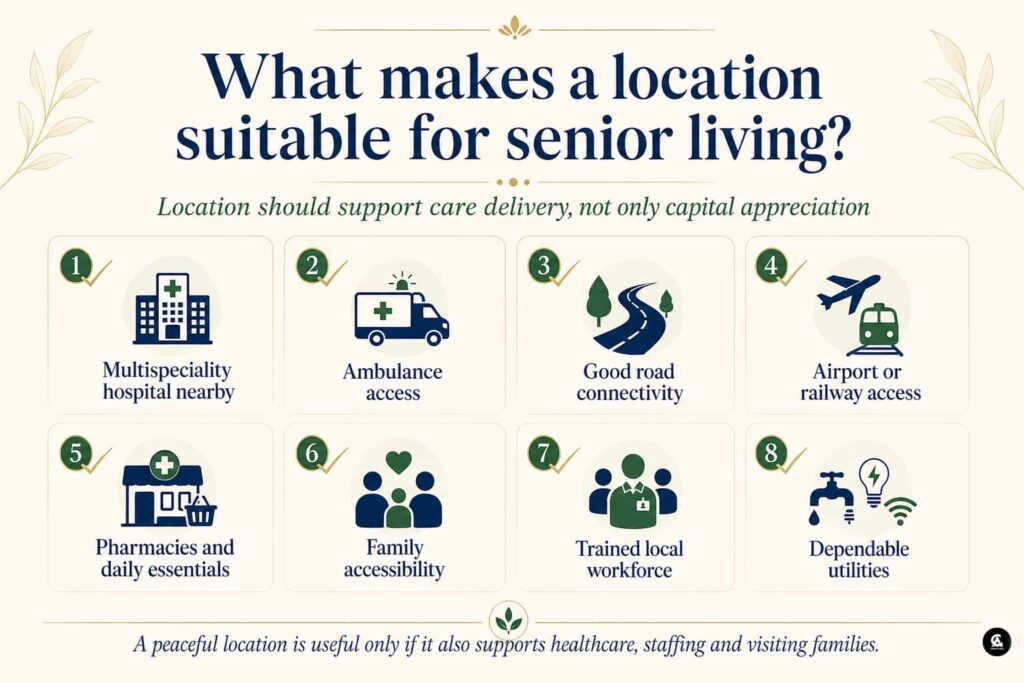

Location matters, but not in the usual way

A quiet location with greenery may appear suitable for senior living.

But peaceful surroundings alone are not enough.

The project also needs:

- a reliable multispeciality hospital;

- ambulance access;

- good road connectivity;

- access to an airport or railway station;

- pharmacies and essential retail;

- dependable electricity and water;

- trained local staff;

- and easy access for visiting family members.

A remote location may reduce the land cost but increase operational difficulties.

The operator may struggle to recruit nurses, caregivers, chefs and other employees.

Hospital proximity should also be checked carefully.

A hospital located nearby is not the same as a formal hospital tie-up. Investors should ask whether an agreement exists and what services it actually covers.

Who should consider a senior living investment?

Senior living may be suitable for investors who:

- understand specialised real estate;

- are comfortable with a long holding period;

- can evaluate the quality of an operator;

- do not depend on immediate resale;

- and are willing to study recurring service costs.

It may be less suitable for investors who:

- require high liquidity;

- expect guaranteed appreciation;

- want complete control over leasing;

- are uncomfortable with rising service charges;

- or are relying only on India’s demographic growth story.

An ageing population can create demand for the sector. It does not guarantee the success of every project.

Investor due-diligence checklist

Before purchasing a senior living property, verify four areas.

Property

Check:

- title and ownership;

- sanctioned land use;

- RERA registration, where applicable;

- approved building plans;

- possession status;

- and occupancy certificate.

Operator

Check:

- operating experience;

- current projects;

- occupancy;

- resident feedback;

- staffing;

- emergency systems;

- and financial stability.

Financials

Check:

- total acquisition cost;

- maintenance charges;

- monthly service fees;

- escalation formula;

- actual rent received;

- vacancy history;

- and net rental yield.

Exit

Check:

- resale rules;

- age restrictions;

- transfer charges;

- subletting conditions;

- operator approval;

- and buyback provisions.

The emotional side of the investment

In an investment spreadsheet, a senior living unit may appear as another asset with a purchase price, rental yield and expected appreciation.

For the person occupying it, the same unit may become the last major home chosen in life.

The resident may be leaving a house filled with decades of memories. The family may be trusting the operator to respond during a late-night emergency. A son or daughter living abroad may be paying not only for accommodation, but also for peace of mind.

This is why senior living cannot be evaluated only through financial returns.

The product carries responsibility for:

- dignity;

- independence;

- safety;

- companionship;

- and care.

Projects that understand this responsibility may build long-term trust.

Projects that treat senior living only as premium real estate may struggle once residents begin experiencing the daily operations.

Carpet Area view

India’s ageing population creates a credible long-term requirement for organised senior housing.

Limited supply and low organised-market penetration also indicate that the sector has substantial room to grow.

But demographic growth does not guarantee investment success.

A senior living project may still struggle because of:

- an unsuitable location;

- unrealistic pricing;

- poor operations;

- weak healthcare support;

- unaffordable service charges;

- or limited resale demand.

A conventional residential investor primarily evaluates the property.

A senior living investor must evaluate three things together:

The property, the operator and the care ecosystem.

When one of these is weak, the investment may lose its long-term appeal.

Final assessment

Senior living is developing into an important specialised segment of Indian real estate.

The sector has a strong demand story and considerable long-term potential. But it is not a simple buy-and-wait investment.

Returns may depend on:

- project location;

- operating quality;

- occupancy;

- service affordability;

- healthcare systems;

- rental structure;

- and exit flexibility.

The smartest investor will not ask only:

How much could this property appreciate?

The better question is:

Will seniors and their families continue trusting this community ten years from now?

That trust—not the building alone—will determine the project’s real long-term value.

Sources:-

- UNFPA, India Ageing Report 2023:

https://india.unfpa.org/sites/default/files/pub-pdf/20230926_india_ageing_report_2023_web_version_.pdf - JLL and Association of Senior Living India, Elevating the Golden Years:

https://www.jll.co.in/en/trends-and-insights/research/elevating-the-golden-years-a-report-on-indias-senior-living-market-landscape - CBRE India, Golden Opportunities from the Silver Economy:

https://www.cbre.co.in/insights/reports/golden-opportunities-from-the-silver-economy-analysing-the-future-of-india-s-senior-care

Leave a Reply